In 2022, Elon Musk pulled off one of the boldest business moves in modern times. He bought Twitter (now X) for $44 billion. But here’s what most people missed. He didn’t sell a single asset of his to fund it. Instead, he borrowed billions against them.

While most of us would sell our assets to raise money, Musk did just the opposite. He used his asset as collateral, took out a loan, and bought Twitter (now X). In this process, he avoided paying any capital gains tax, his Tesla shares continued to appreciate in value, and he retained control of his company.

That’s the secret strategy of the ultra-wealthy, and if you feel that it's only for them, then you are wrong. With the right strategy and planning, anyone can use this policy to his benefit and gain massively out of it, but it's not that simple either.

In this newsletter,We will discuss everything about the following

What this strategy really means

How do people like Musk and Ambani use it?

The tools that make it possible (and accessible)

The fine line between smart leverage and financial ruin

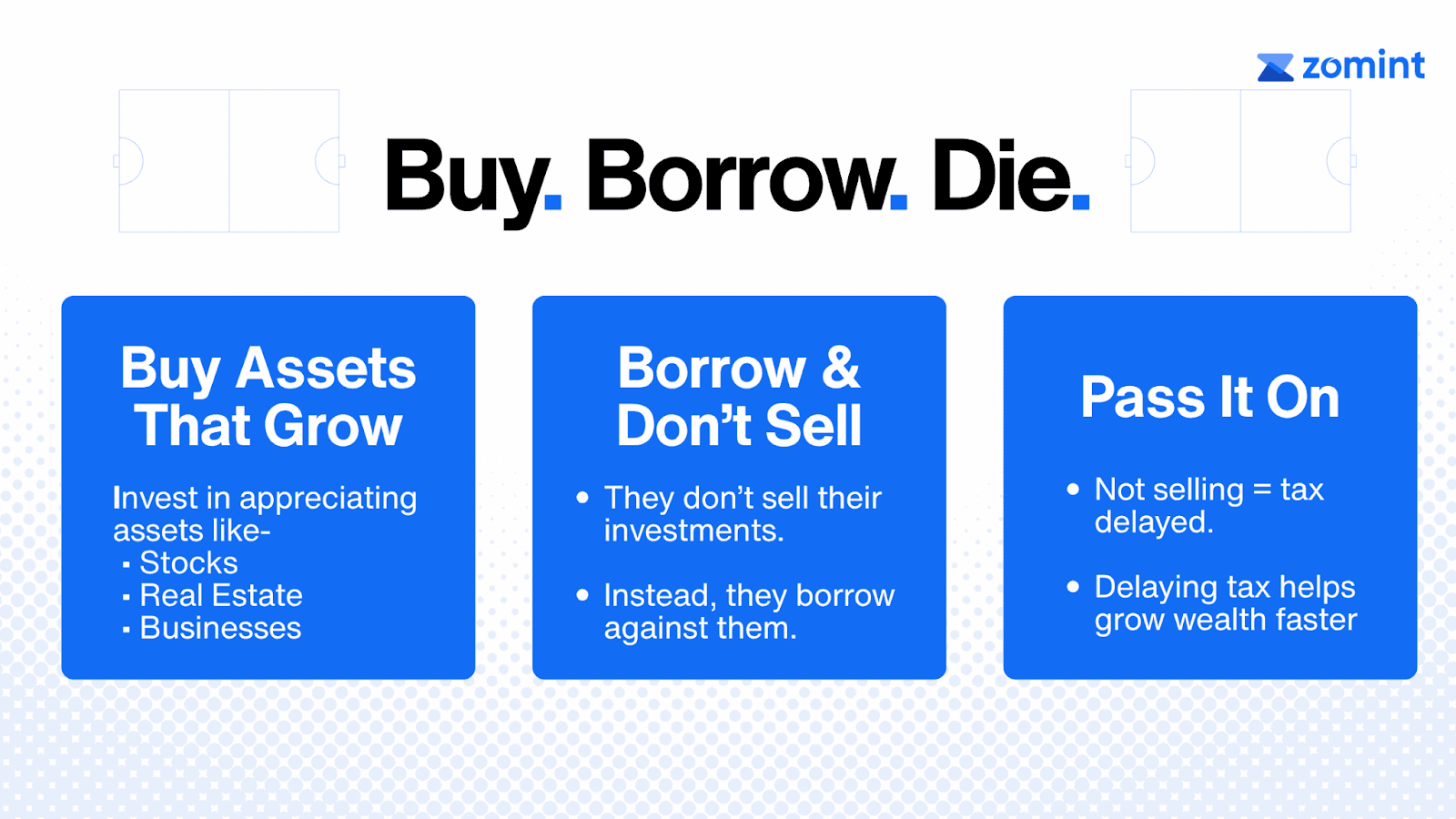

The Strategy Buy. Borrow. Die.

What Elon Musk did while buying Twitter wasn’t something random. It’s part of a common strategy used by many wealthy individuals. The strategy is known as buy. Borrow. Die, and the concept behind it is quite straightforward.

Step 1: Buy assets that grow.

Wealthy people don’t keep a lot of money in cash. Instead, they invest in things that increase in value over time, like stocks, real estate, or businesses

Step 2: Borrow instead of selling.

When they need money, they don’t sell their investments; instead, they borrow against their investments, like taking a loan against mutual funds, shares, or real estate.

Step 3: Pass it on.

When they die, their investments go to their children. In countries like the US, a rule called "step-up" removes the capital gains tax at death. India doesn’t have this rule, but the idea is simple: if you don’t sell your assets, you don’t pay tax right now. And delaying tax can grow your wealth a lot over time.

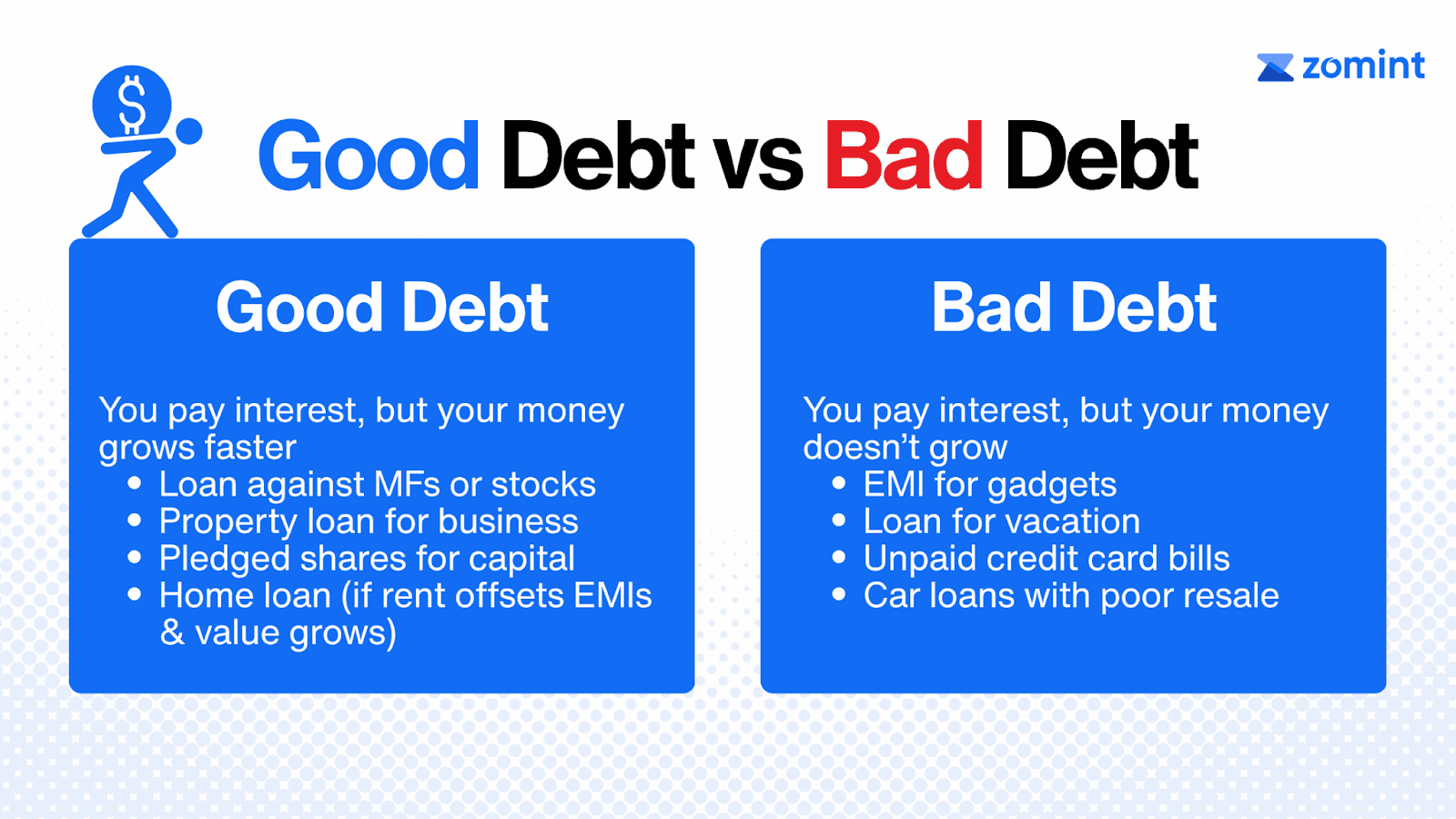

Good Debt vs. Bad Debt

Most of us fear Debt ,and for good reason.We’ve seen how credit card bills spiral out of control, how EMIs eat into salaries, and how one wrong loan can derail your entire financial future. So it’s natural to associate debt with stress.

But the truth is, not all debts are harmful. In fact, the ultra-wealthy use debt all the time,but they use it differently.

There are two types of debt: bad debt and good debt.

Bad Debt: You pay interest, and your money doesn’t grow.

Bad debt is usually taken to buy something that loses value over time. This is the kind of debt most people are familiar with. Examples include

Buying a phone or laptop on EMI

Taking a personal loan for a vacation

Credit card spending you can’t repay in full

Car loans with no resale value

These don’t generate income or build long-term value. They’re the silent killers of wealth creation.

Good Debt: You pay interest, but your money grows faster.

This is the kind of debt the wealthy prefer. It’s backed by assets and allows them to stay invested while still accessing cash.

Examples include

Borrowing against mutual funds or stocks instead of selling them

Taking a loan against property to invest in a business

Using pledged shares to raise working capital

Taking a home loan (when the property appreciates and rent offsets EMIs)

Here, the logic is simple:

If your investment is growing at, say, 12% per year, and your loan costs you 8%, you’re still net positive. You stay invested, defer taxes, and your money works harder than the interest you’re paying.

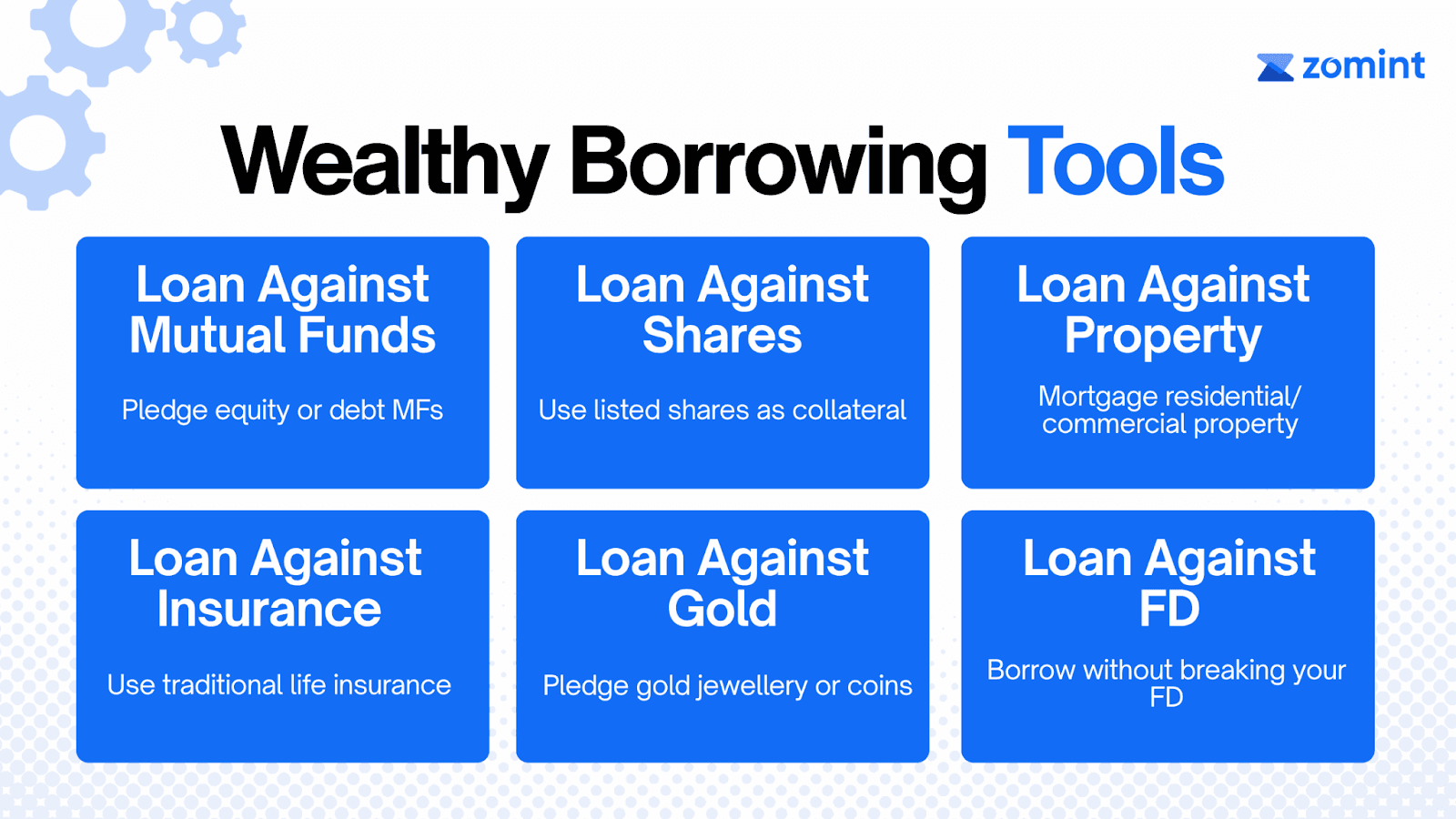

The Tools the Wealthy Use to Borrow Without Selling

So far we’ve seen that borrowing against assets can be smarter than selling them if done carefully. Now let’s explore five common methods wealthy individuals use, which are becoming increasingly accessible to regular investors as well.

Loan Against Mutual Funds (LAMF)

If you have mutual fund units (especially debt or equity funds), you can pledge them to a bank or NBFC and get a loan — usually up to 50–70% of their value.

Loan Against Shares (LAS)

Just like mutual funds, shares can also be used as collateral. You get a credit limit based on their current value, and interest is charged only when you use it.

Loan Against Property (LAP)

This is a popular method in India. You mortgage a residential or commercial property and borrow against its value — usually up to 50–60%.

Loan Against Insurance (LAI)

If you have a traditional life insurance plan (like endowment or whole life policies), you can borrow against its surrender value.

Loan Against Gold (LAG)

This one’s simple and widely used. You pledge your gold jewellery or coins and get a quick loan, often with low interest.

Loan Against FD (LAFD)

Loan Against FD (LAFD) lets you access funds without breaking your Fixed Deposit. You can borrow up to 90% of the FD’s value at an interest rate typically 1–2% above the FD rate. There’s no prepayment penalty, making it a flexible option for quick liquidity while still earning returns on your deposit.

When Borrowing Backfires

Everything we’ve walked through can work wonders , if you apply it with discipline and keep a clear eye on the risks. Borrowing can speed up growth, but it can derail you just as easily when greed or neglect takes over.

When you pledge shares, mutual funds, or property as collateral, they're exposed to market fluctuations. If markets suddenly drop and your collateral loses value, lenders may issue a margin call, requiring you to either repay part of the loan or add more collateral. If you can’t, the lender can liquidate your holdings at a loss, damaging your financial future.

We’ve seen this happen in real life to large corporations with assets worth billions of rupees:-

Anil Ambani’s group pledged shares aggressively. When their stock prices fell, lenders dumped the shares and the empire began to crumble.

Jet Airways kept borrowing to expand without solid financials. Eventually, it had to ground itself permanently buried under its own debt.

The Takeaway — Borrowing Isn’t the Enemy. Misusing It Is.

If you have read this far, you now understand something that most people never do. Debt isn’t always a danger. In fact, it is one of the most powerful tools you can use to compound your wealth. The key is knowing exactly when to use it and when to avoid it.

Just ask yourself these questions

Will my assets keep growing while I'm borrowing against them?

Is the interest I'll pay lower than the returns I expect?

Am I borrowing with a clear plan rather than seeking a short-term fix?

And If all the answers are "yes," then you are not misusing debt; rather, you are managing your money purposefully .

Take control of your financial future — with expert guidance that puts you first.

At Zomint, your portfolio is reviewed and managed by SEBI-registered experts who focus on long-term results, not short-term noise.

👉 Get a free personalized portfolio review today at zomint.com

In 2022, Elon Musk pulled off one of the boldest business moves in modern times. He bought Twitter (now X) for $44 billion. But here’s what most people missed. He didn’t sell a single asset of his to fund it. Instead, he borrowed billions against them.

While most of us would sell our assets to raise money, Musk did just the opposite. He used his asset as collateral, took out a loan, and bought Twitter (now X). In this process, he avoided paying any capital gains tax, his Tesla shares continued to appreciate in value, and he retained control of his company.

That’s the secret strategy of the ultra-wealthy, and if you feel that it's only for them, then you are wrong. With the right strategy and planning, anyone can use this policy to his benefit and gain massively out of it, but it's not that simple either.

In this newsletter,We will discuss everything about the following

What this strategy really means

How do people like Musk and Ambani use it?

The tools that make it possible (and accessible)

The fine line between smart leverage and financial ruin

The Strategy Buy. Borrow. Die.

What Elon Musk did while buying Twitter wasn’t something random. It’s part of a common strategy used by many wealthy individuals. The strategy is known as buy. Borrow. Die, and the concept behind it is quite straightforward.

Step 1: Buy assets that grow.

Wealthy people don’t keep a lot of money in cash. Instead, they invest in things that increase in value over time, like stocks, real estate, or businesses

Step 2: Borrow instead of selling.

When they need money, they don’t sell their investments; instead, they borrow against their investments, like taking a loan against mutual funds, shares, or real estate.

Step 3: Pass it on.

When they die, their investments go to their children. In countries like the US, a rule called "step-up" removes the capital gains tax at death. India doesn’t have this rule, but the idea is simple: if you don’t sell your assets, you don’t pay tax right now. And delaying tax can grow your wealth a lot over time.

Good Debt vs. Bad Debt

Most of us fear Debt ,and for good reason.We’ve seen how credit card bills spiral out of control, how EMIs eat into salaries, and how one wrong loan can derail your entire financial future. So it’s natural to associate debt with stress.

But the truth is, not all debts are harmful. In fact, the ultra-wealthy use debt all the time,but they use it differently.

There are two types of debt: bad debt and good debt.

Bad Debt: You pay interest, and your money doesn’t grow.

Bad debt is usually taken to buy something that loses value over time. This is the kind of debt most people are familiar with. Examples include

Buying a phone or laptop on EMI

Taking a personal loan for a vacation

Credit card spending you can’t repay in full

Car loans with no resale value

These don’t generate income or build long-term value. They’re the silent killers of wealth creation.

Good Debt: You pay interest, but your money grows faster.

This is the kind of debt the wealthy prefer. It’s backed by assets and allows them to stay invested while still accessing cash.

Examples include

Borrowing against mutual funds or stocks instead of selling them

Taking a loan against property to invest in a business

Using pledged shares to raise working capital

Taking a home loan (when the property appreciates and rent offsets EMIs)

Here, the logic is simple:

If your investment is growing at, say, 12% per year, and your loan costs you 8%, you’re still net positive. You stay invested, defer taxes, and your money works harder than the interest you’re paying.

The Tools the Wealthy Use to Borrow Without Selling

So far we’ve seen that borrowing against assets can be smarter than selling them if done carefully. Now let’s explore five common methods wealthy individuals use, which are becoming increasingly accessible to regular investors as well.

Loan Against Mutual Funds (LAMF)

If you have mutual fund units (especially debt or equity funds), you can pledge them to a bank or NBFC and get a loan — usually up to 50–70% of their value.

Loan Against Shares (LAS)

Just like mutual funds, shares can also be used as collateral. You get a credit limit based on their current value, and interest is charged only when you use it.

Loan Against Property (LAP)

This is a popular method in India. You mortgage a residential or commercial property and borrow against its value — usually up to 50–60%.

Loan Against Insurance (LAI)

If you have a traditional life insurance plan (like endowment or whole life policies), you can borrow against its surrender value.

Loan Against Gold (LAG)

This one’s simple and widely used. You pledge your gold jewellery or coins and get a quick loan, often with low interest.

Loan Against FD (LAFD)

Loan Against FD (LAFD) lets you access funds without breaking your Fixed Deposit. You can borrow up to 90% of the FD’s value at an interest rate typically 1–2% above the FD rate. There’s no prepayment penalty, making it a flexible option for quick liquidity while still earning returns on your deposit.

When Borrowing Backfires

Everything we’ve walked through can work wonders , if you apply it with discipline and keep a clear eye on the risks. Borrowing can speed up growth, but it can derail you just as easily when greed or neglect takes over.

When you pledge shares, mutual funds, or property as collateral, they're exposed to market fluctuations. If markets suddenly drop and your collateral loses value, lenders may issue a margin call, requiring you to either repay part of the loan or add more collateral. If you can’t, the lender can liquidate your holdings at a loss, damaging your financial future.

We’ve seen this happen in real life to large corporations with assets worth billions of rupees:-

Anil Ambani’s group pledged shares aggressively. When their stock prices fell, lenders dumped the shares and the empire began to crumble.

Jet Airways kept borrowing to expand without solid financials. Eventually, it had to ground itself permanently buried under its own debt.

The Takeaway — Borrowing Isn’t the Enemy. Misusing It Is.

If you have read this far, you now understand something that most people never do. Debt isn’t always a danger. In fact, it is one of the most powerful tools you can use to compound your wealth. The key is knowing exactly when to use it and when to avoid it.

Just ask yourself these questions

Will my assets keep growing while I'm borrowing against them?

Is the interest I'll pay lower than the returns I expect?

Am I borrowing with a clear plan rather than seeking a short-term fix?

And If all the answers are "yes," then you are not misusing debt; rather, you are managing your money purposefully .

Take control of your financial future — with expert guidance that puts you first.

At Zomint, your portfolio is reviewed and managed by SEBI-registered experts who focus on long-term results, not short-term noise.

👉 Get a free personalized portfolio review today at zomint.com