Gold has been on a remarkable run. In India, prices have climbed from around ₹6,000 per 10 grams in 2005 to over ₹1,00,000 in 2025, a jump of more than 15x in just two decades. Last year, gold delivered 28% returns, followed by another 26% surge in the first half of 2025.

This explosive growth has reignited investor interest. The question now is clear: Should you still buy gold in 2025? And if so, what's the smartest way to do it?

In this article, we'll break down the best ways to invest in gold with real-life examples, explain the key tax implications, and provide a clear analysis of whether gold still deserves a place in your portfolio.

Why Gold?

1. Cultural and Household Significance

In India, gold is deeply embedded in tradition. Indians collectively hold over 25,000 tonnes of gold, making it one of the largest private reserves in the world. More than just jewelry, gold is a symbol of prosperity, inheritance, and financial security.

2. Safe-Haven and Diversification Role

Globally, gold serves as the ultimate safe haven. During crises, its value tends to rise when other assets fall.

In 2008, when global equity markets crashed, gold's value rose by nearly 25%.

In 2020, during the COVID turmoil, gold touched record highs in India.

3. Central Banks and Global Demand

Central banks play a critical, often overlooked role. Their global official gold reserves are projected to reach 36,000 tonnes in 2025. This shift highlights rising concerns about inflation, currency debasement, and geopolitical risks.

For individual investors, the signal is clear: gold remains a strategic hedge and a long-term insurance policy.

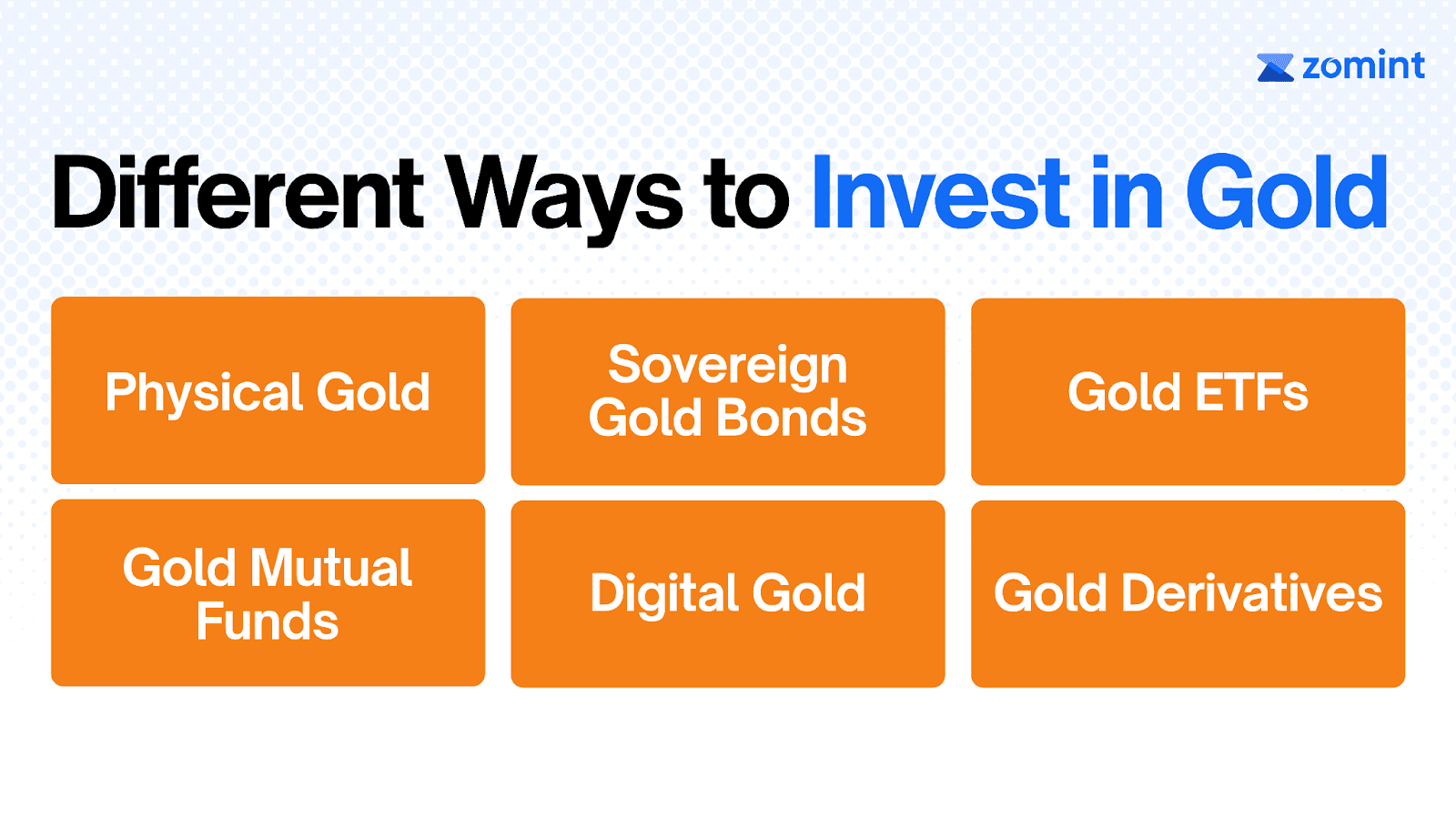

Different Ways to Invest in Gold

1. Physical Gold (Jewelry, Coins, Bars)

Pros: Direct ownership, trusted for generations, and carries cultural value.

Cons: High making charges, 3% GST, storage and insurance costs, and can be difficult to sell.

Tax:

Short-term (up to 24 months): Profits are added to your income and taxed at your slab rate.

Long-term (over 24 months): Taxed at a flat 12.5% with indexation benefit.

2. Sovereign Gold Bonds (SGBs)

Pros: Issued by the RBI, government-backed, earns 2.5% yearly interest, no capital gains tax if held to maturity (8 years), and since fresh issuance is closed, it can only be bought from the secondary market.

Cons: Low liquidity; selling before maturity can be difficult.

Tax: Interest is taxed as per your income slab. If held until maturity, there is no capital gains tax.

3. Gold ETFs (Exchange-Traded Funds)

Pros: Highly liquid, transparent pricing, no storage issues, and low costs.

Cons: Requires a Demat account, plus small brokerage and fund charges.

Tax:

Short-term (up to 24 months): Taxed at your slab rate.

Long-term (over 24 months): Taxed at a 12.5% rate.

4. Gold Mutual Funds

Pros: Easy to start with SIPs, no Demat account needed, and managed by professionals.

Cons: Higher expense ratios than ETFs; Net Asset Value (NAV) updates only once a day.

Tax:

Short-term (up to 24 months): Taxed at your slab rate.

Long-term (over 24 months): Taxed at a 12.5% rate.

5. Digital Gold

Pros: Can start with as little as ₹1, available 24/7, backed by 24K pure gold, and you can request physical delivery.

Cons: Not regulated by SEBI/RBI, 3% GST, plus a 3–5% buy/sell spread, and storage fees for long-term holding.

Tax:

Short-term (up to 24 months): Taxed at your slab rate.

Long-term (over 24 months): Taxed at a 12.5% rate.

6. Gold Derivatives (Futures & Options)

Pros: Extremely liquid, can profit in both rising and falling markets, and allows for leverage.

Cons: Highly risky, contracts expire, and not suitable for most investors.

Tax: Treated as business/speculative income, added to your income, and taxed at your slab rate. No long-term tax benefits.

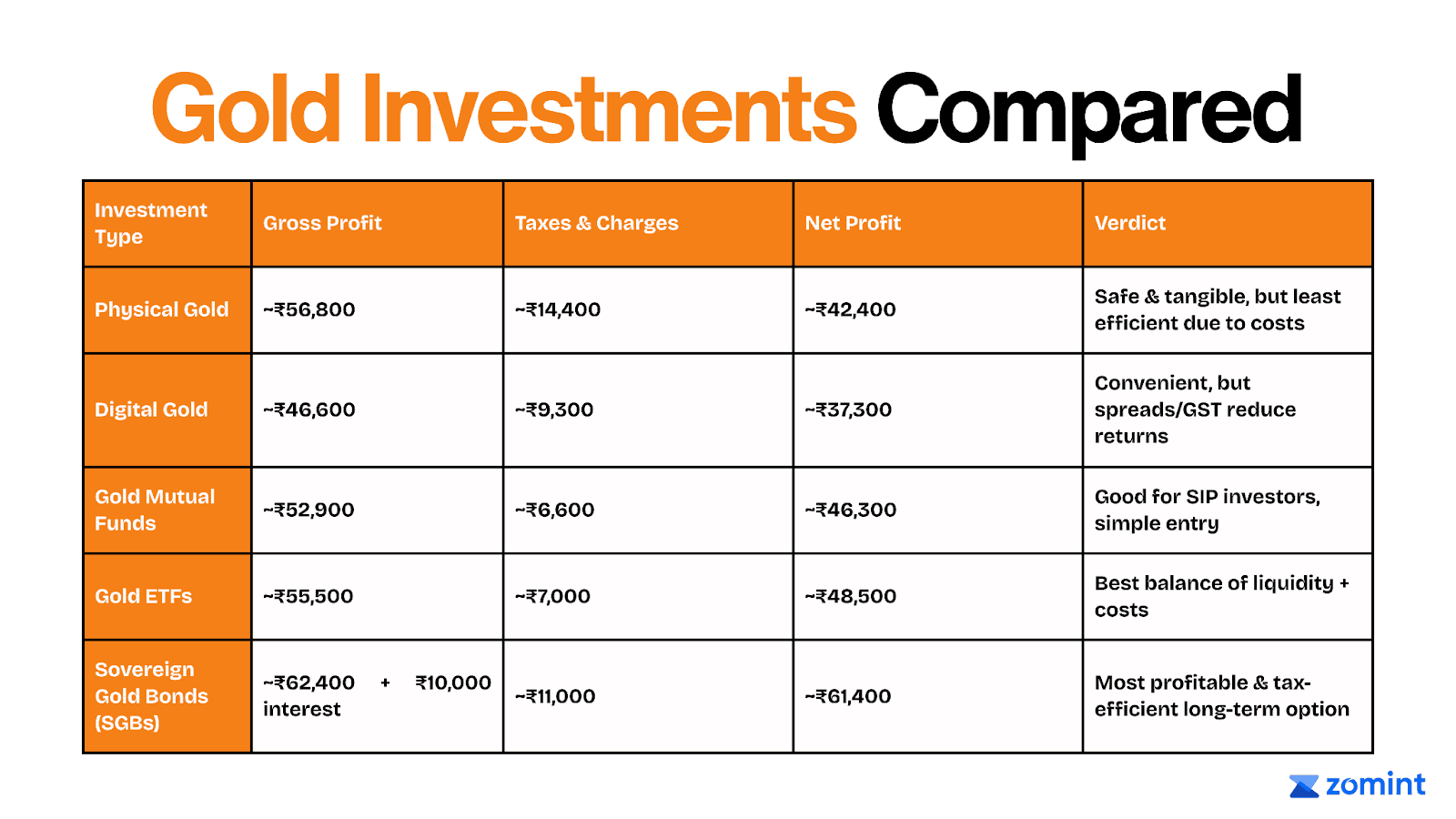

Gold Investment Comparison

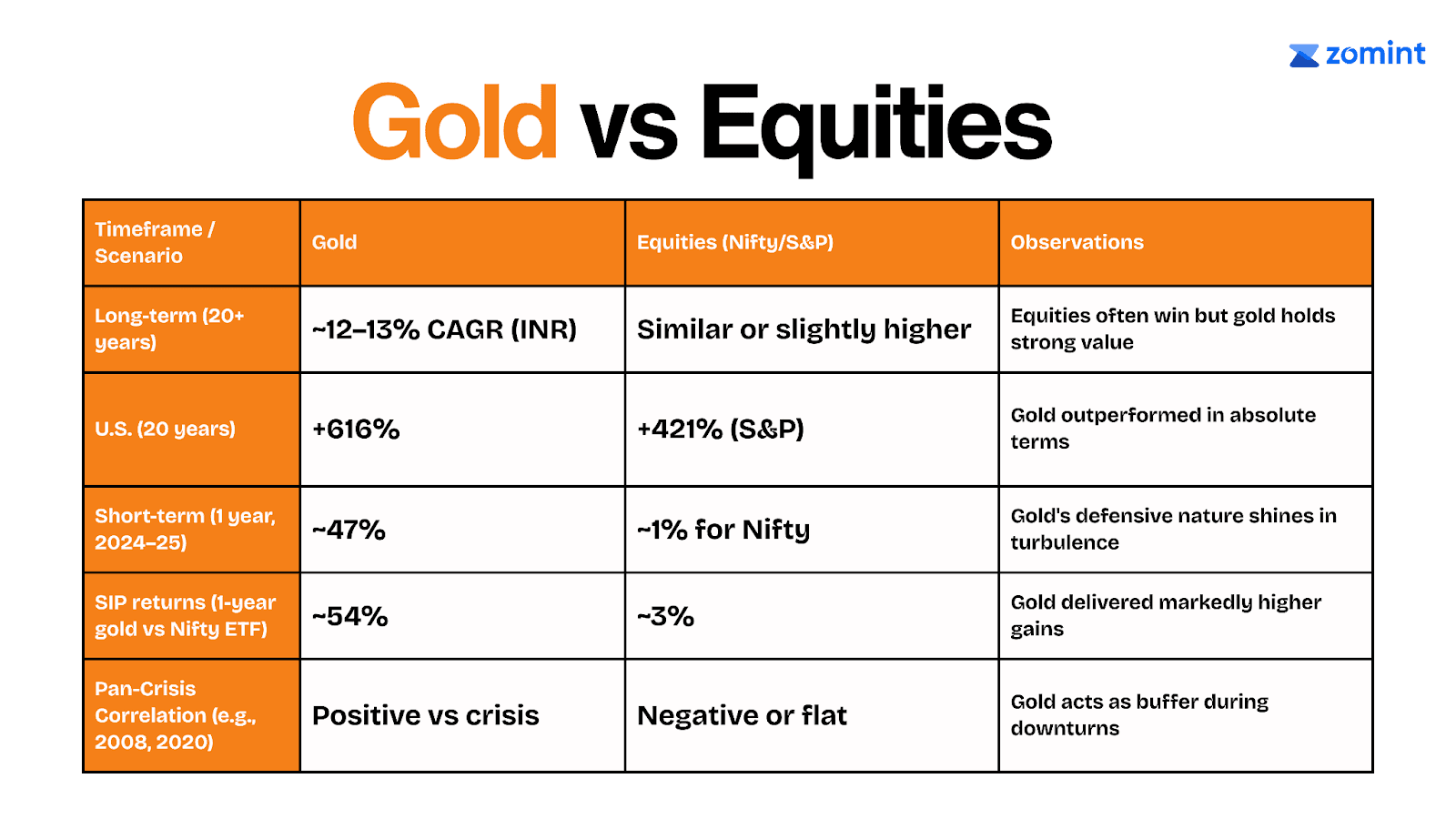

Gold vs. Equities: Who Wins When?

Long-Term Trends

In India, gold and Nifty both delivered ~12–13% CAGR over 20 years.

Globally, gold rose 616%, beating the S&P 500’s 421%.

Since 2000, gold has gained 2,000% vs. Nifty’s 1,470%, showing its strength as a preserver of wealth.

Short-Term & Crisis Advantage

2024–25: Gold surged 47%, while Nifty rose just 1%.

1-year SIPs: Gold ETFs returned 54% vs. Nifty’s 3%.

In crises (2008 crash, 2020 pandemic), gold climbed while equities tumbled.

Gold Portfolio Allocation Strategy

Given its dual role as a safe haven and a long-term wealth preserver, most wealth advisors recommend keeping 10–15% of your total portfolio in gold.

This allocation provides powerful diversification benefits without overexposing you to a non-productive asset. The golden rule for investors is simple:

Think of gold as an insurance policy, not a primary growth driver.

It is designed to protect your wealth during crises, not to generate the same compounding returns as equities.

Ultimately, the smartest allocation is one that protects your downside without compromising your upside.

Should You Invest in Gold in 2025?

To the question, “Should I still invest in gold in 2025?” The answer is yes, but wisely.

Gold is not about chasing quick gains; it's about adding stability, protection, and balance to your portfolio. It’s an essential strategic asset for every investor.

If you're still unsure about the best way to invest in gold this year, consider getting a personalized strategy for your portfolio. To get started, you can book a free call with Zomint’s SEBI-regulated experts.

Disclaimer: This article is for educational purposes only and should not be considered as investment advice. Investing in gold or any financial instrument carries risks. Please consult Zomint’s SEBI-registered experts before making any investment decisions.

Gold has been on a remarkable run. In India, prices have climbed from around ₹6,000 per 10 grams in 2005 to over ₹1,00,000 in 2025, a jump of more than 15x in just two decades. Last year, gold delivered 28% returns, followed by another 26% surge in the first half of 2025.

This explosive growth has reignited investor interest. The question now is clear: Should you still buy gold in 2025? And if so, what's the smartest way to do it?

In this article, we'll break down the best ways to invest in gold with real-life examples, explain the key tax implications, and provide a clear analysis of whether gold still deserves a place in your portfolio.

Why Gold?

1. Cultural and Household Significance

In India, gold is deeply embedded in tradition. Indians collectively hold over 25,000 tonnes of gold, making it one of the largest private reserves in the world. More than just jewelry, gold is a symbol of prosperity, inheritance, and financial security.

2. Safe-Haven and Diversification Role

Globally, gold serves as the ultimate safe haven. During crises, its value tends to rise when other assets fall.

In 2008, when global equity markets crashed, gold's value rose by nearly 25%.

In 2020, during the COVID turmoil, gold touched record highs in India.

3. Central Banks and Global Demand

Central banks play a critical, often overlooked role. Their global official gold reserves are projected to reach 36,000 tonnes in 2025. This shift highlights rising concerns about inflation, currency debasement, and geopolitical risks.

For individual investors, the signal is clear: gold remains a strategic hedge and a long-term insurance policy.

Different Ways to Invest in Gold

1. Physical Gold (Jewelry, Coins, Bars)

Pros: Direct ownership, trusted for generations, and carries cultural value.

Cons: High making charges, 3% GST, storage and insurance costs, and can be difficult to sell.

Tax:

Short-term (up to 24 months): Profits are added to your income and taxed at your slab rate.

Long-term (over 24 months): Taxed at a flat 12.5% with indexation benefit.

2. Sovereign Gold Bonds (SGBs)

Pros: Issued by the RBI, government-backed, earns 2.5% yearly interest, no capital gains tax if held to maturity (8 years), and since fresh issuance is closed, it can only be bought from the secondary market.

Cons: Low liquidity; selling before maturity can be difficult.

Tax: Interest is taxed as per your income slab. If held until maturity, there is no capital gains tax.

3. Gold ETFs (Exchange-Traded Funds)

Pros: Highly liquid, transparent pricing, no storage issues, and low costs.

Cons: Requires a Demat account, plus small brokerage and fund charges.

Tax:

Short-term (up to 24 months): Taxed at your slab rate.

Long-term (over 24 months): Taxed at a 12.5% rate.

4. Gold Mutual Funds

Pros: Easy to start with SIPs, no Demat account needed, and managed by professionals.

Cons: Higher expense ratios than ETFs; Net Asset Value (NAV) updates only once a day.

Tax:

Short-term (up to 24 months): Taxed at your slab rate.

Long-term (over 24 months): Taxed at a 12.5% rate.

5. Digital Gold

Pros: Can start with as little as ₹1, available 24/7, backed by 24K pure gold, and you can request physical delivery.

Cons: Not regulated by SEBI/RBI, 3% GST, plus a 3–5% buy/sell spread, and storage fees for long-term holding.

Tax:

Short-term (up to 24 months): Taxed at your slab rate.

Long-term (over 24 months): Taxed at a 12.5% rate.

6. Gold Derivatives (Futures & Options)

Pros: Extremely liquid, can profit in both rising and falling markets, and allows for leverage.

Cons: Highly risky, contracts expire, and not suitable for most investors.

Tax: Treated as business/speculative income, added to your income, and taxed at your slab rate. No long-term tax benefits.

Gold Investment Comparison

Gold vs. Equities: Who Wins When?

Long-Term Trends

In India, gold and Nifty both delivered ~12–13% CAGR over 20 years.

Globally, gold rose 616%, beating the S&P 500’s 421%.

Since 2000, gold has gained 2,000% vs. Nifty’s 1,470%, showing its strength as a preserver of wealth.

Short-Term & Crisis Advantage

2024–25: Gold surged 47%, while Nifty rose just 1%.

1-year SIPs: Gold ETFs returned 54% vs. Nifty’s 3%.

In crises (2008 crash, 2020 pandemic), gold climbed while equities tumbled.

Gold Portfolio Allocation Strategy

Given its dual role as a safe haven and a long-term wealth preserver, most wealth advisors recommend keeping 10–15% of your total portfolio in gold.

This allocation provides powerful diversification benefits without overexposing you to a non-productive asset. The golden rule for investors is simple:

Think of gold as an insurance policy, not a primary growth driver.

It is designed to protect your wealth during crises, not to generate the same compounding returns as equities.

Ultimately, the smartest allocation is one that protects your downside without compromising your upside.

Should You Invest in Gold in 2025?

To the question, “Should I still invest in gold in 2025?” The answer is yes, but wisely.

Gold is not about chasing quick gains; it's about adding stability, protection, and balance to your portfolio. It’s an essential strategic asset for every investor.

If you're still unsure about the best way to invest in gold this year, consider getting a personalized strategy for your portfolio. To get started, you can book a free call with Zomint’s SEBI-regulated experts.

Disclaimer: This article is for educational purposes only and should not be considered as investment advice. Investing in gold or any financial instrument carries risks. Please consult Zomint’s SEBI-registered experts before making any investment decisions.