If you didn’t wake up tomorrow, would your family know where your money really is?

Would they know which bank accounts exist, where the property papers are kept,

or how to access your investments and insurance ?

Most of us spend our entire lives working to build financial security, yet very few of us stop to think about how that money will be used, protected, or structured so that it lasts beyond our own lifetime.

But a small circle of ultra-wealthy families has quietly solved this puzzle..

At Zomint, we work closely with many of India’s affluent families. We’ve distilled their wealth-preservation frameworks into practical methods that you can use in your daily life.

If you’ve ever wondered how to make your money last beyond your lifetime -> Continue Reading

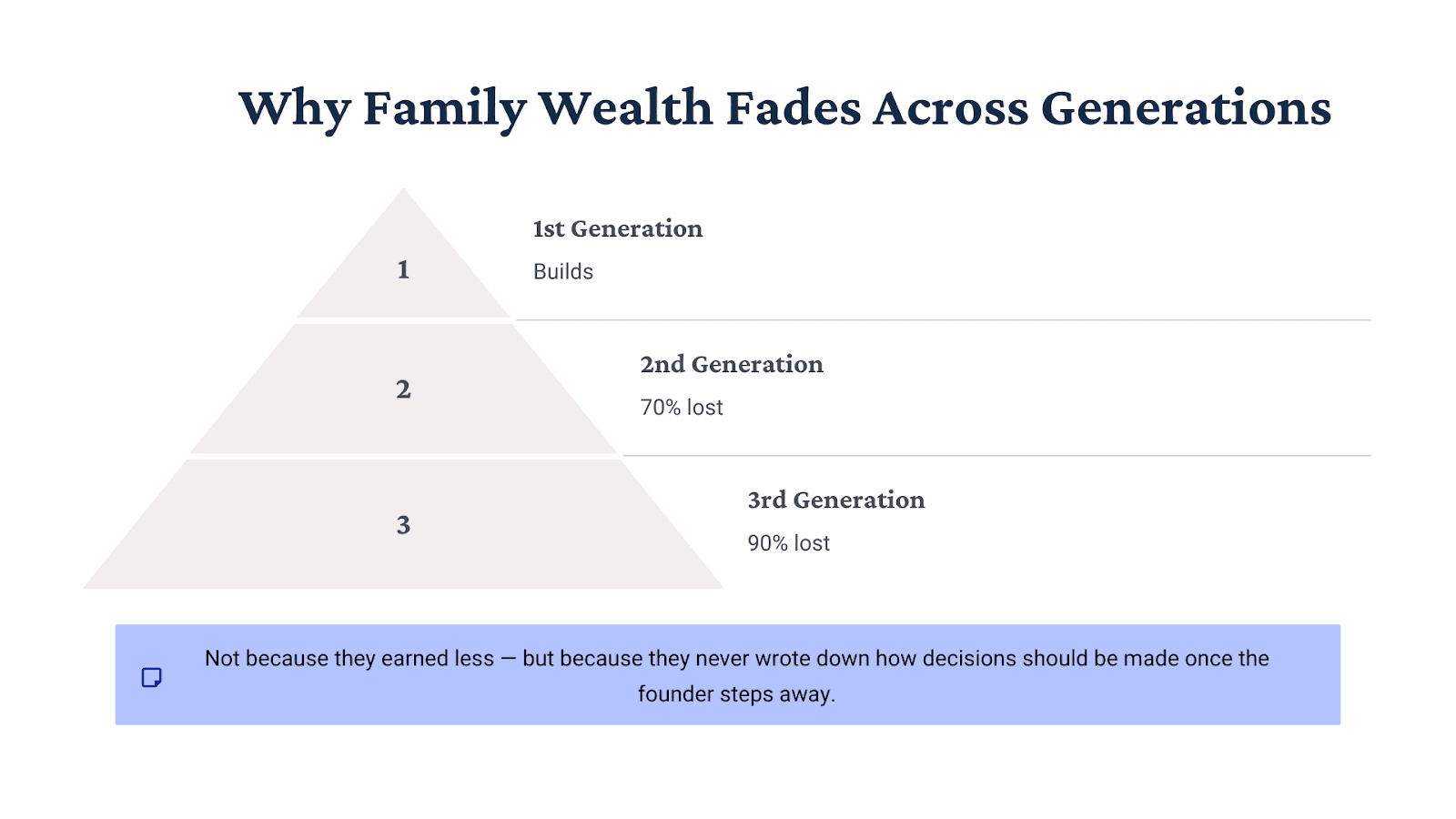

The Real Reason Wealth Disappears

When people think about losing wealth, they imagine a market crash or a bad investment.

But that’s rarely how fortunes fade.Studies show nearly 70% of families lose wealth by the second generation, and 90% by the third—not because they earned less, but because they never documented how decisions should be made once the founder steps away.

That’s why the rich world treats Wealth Governance as their first line of defence—the invisible system that keeps peace, clarity, and control intact.

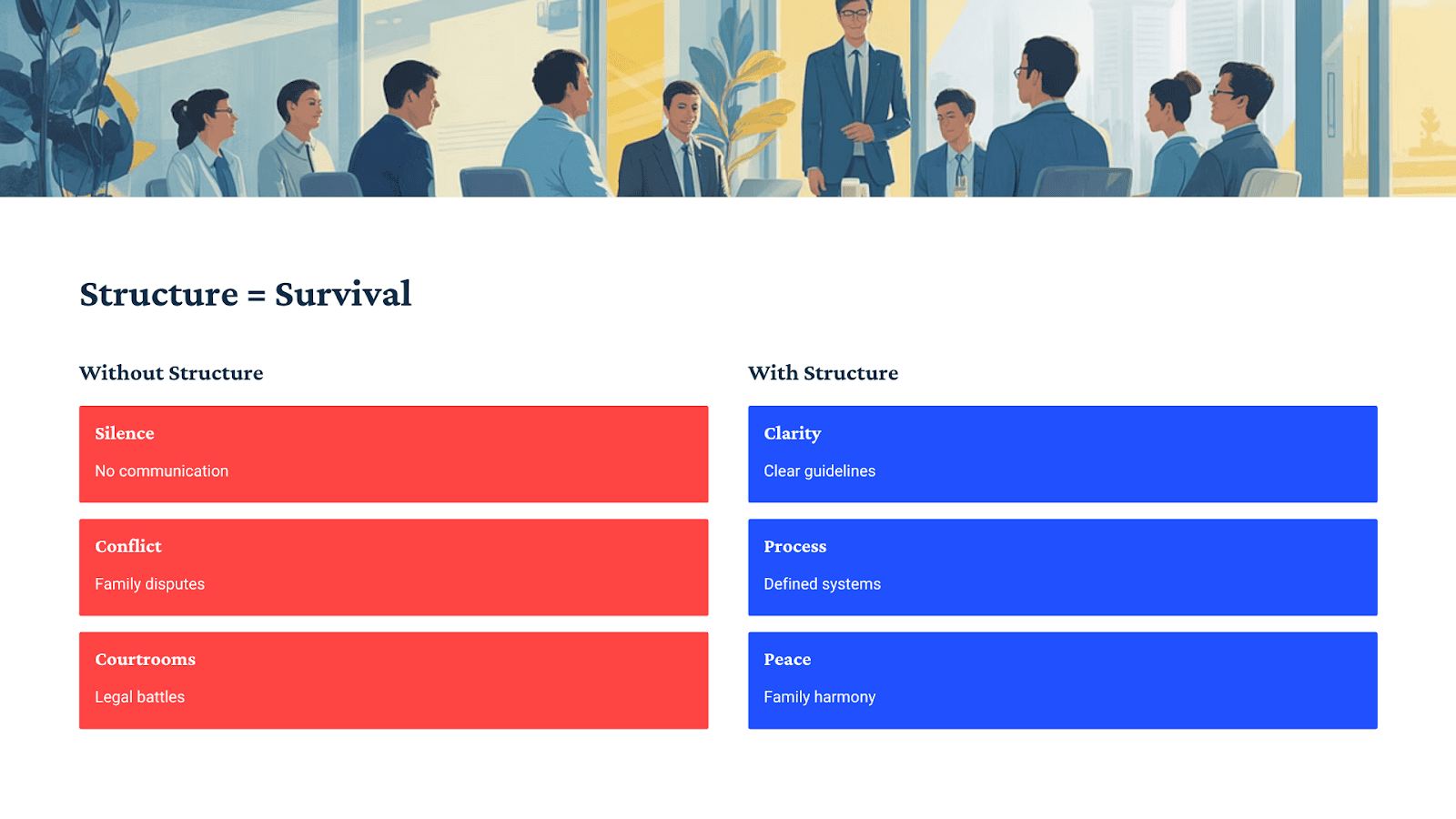

What Happens With and Without Structure?

In the world of money, silence is expensive.

When structure is missing, success turns fragile; siblings stop speaking, partners lose trust, and the empire built through decades becomes a courtroom file.

But where structure exists, clarity replaces confusion.Everyone knows their role, follow process as mentioned, and peace becomes the family’s highest return.

That’s the quiet difference between the rich who stay rich, and those who once were.

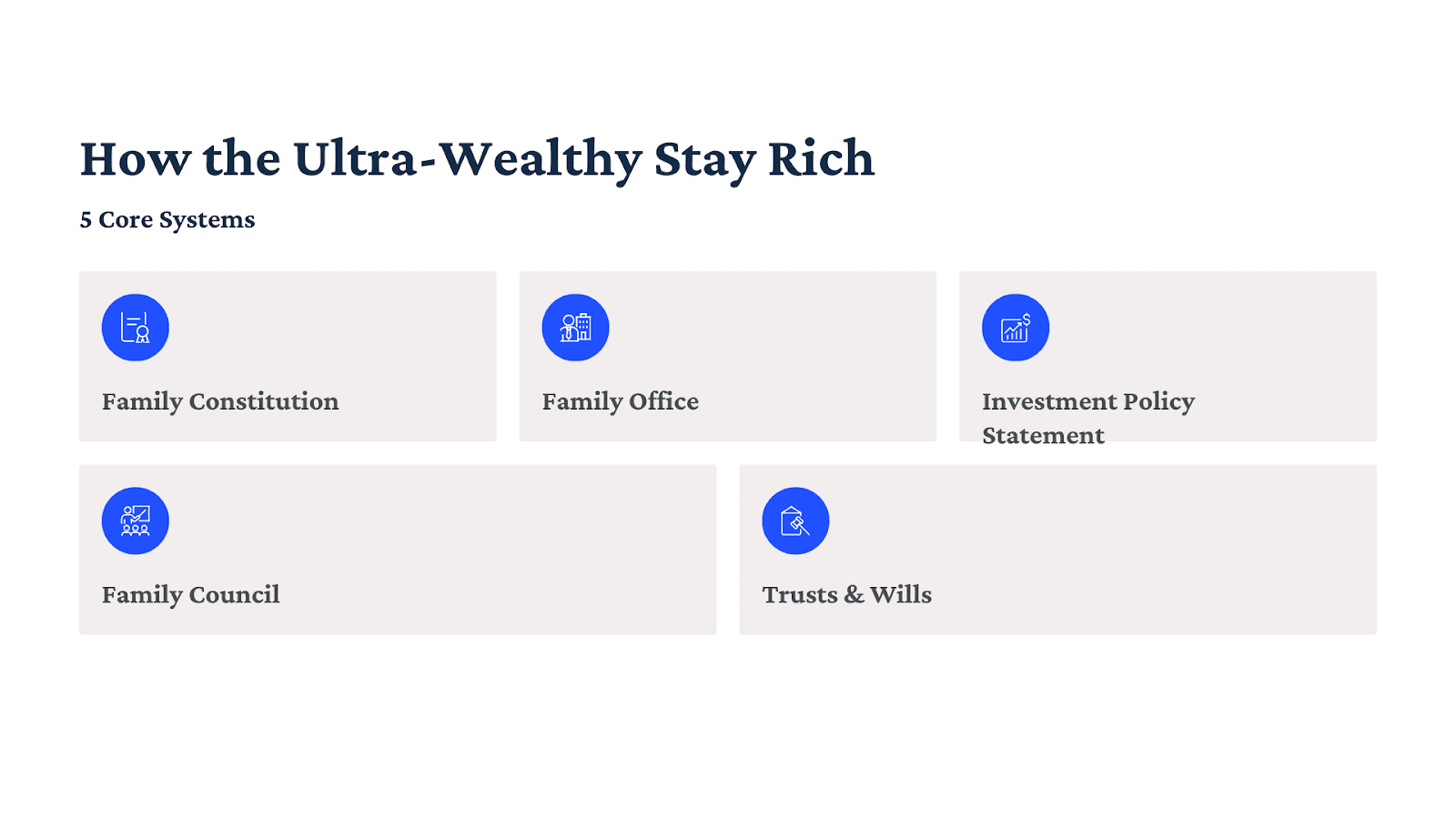

How the Ultra-Wealthy Do It?

The Family Constitution

For many of India’s ultra-rich families, the Family Constitution is the unwritten law that holds everything together — a document that defines how wealth, power, and purpose flow across generations..

The wealthy don’t rely on goodwill or tradition; they rely on clarity. Every successor knows what’s expected, and no major decision is made without referencing “the charter.”

The Family Office

Every billionaire family eventually builds a Family Office—a private firm managing everything from investments and tax to philanthropy and art.

It functions like a CFO for the family: tracking every account, reconciling statements, preparing consolidated reports. Some even employ analysts, lawyers, and psychologists under one roof.This single step turns chaos into structure.

The Investment Policy Statement (IPS)

An Investment Policy Statement (IPS) is your family’s written guide for managing money.It explains your goals, how you’ll invest, how much risk you can take, when to make changes, etc.

For example,It dictates:

Target returns (say, inflation + 3%).

Maximum drawdown tolerated (for example 20%).

Asset-class limits and liquidity needs.

When markets fall, they don’t call the broker, they open the IPS. It keeps billion-dollar portfolios from reacting emotionally.

The Family Council

Ultra-rich families don’t let money talk only at funerals. They hold quarterly councils, separate from business boardrooms, to review:

Family balance sheets and cash needs.

Education of the next generation.

Philanthropy and legacy projects.

Younger members sit in as observers, learning early how wealth is managed. It institutionalizes communication and keeps emotions from turning into litigation.

Trusts & Wills

The ultra-wealthy never leave inheritance to emotion. They plan every transfer , what goes to whom, when, and how and that to long before it becomes urgent.

They use:

Family Trusts to hold assets across generations.

Buy-sell agreements to manage exits or deaths.

Registered wills that complement the trust structure.

For Ultra Wealthy families, these five frameworks are not fancy paperwork , they’re risk-management systems for money and relationships. Each one converts uncertainty into process, emotion into policy, and wealth into legacy.

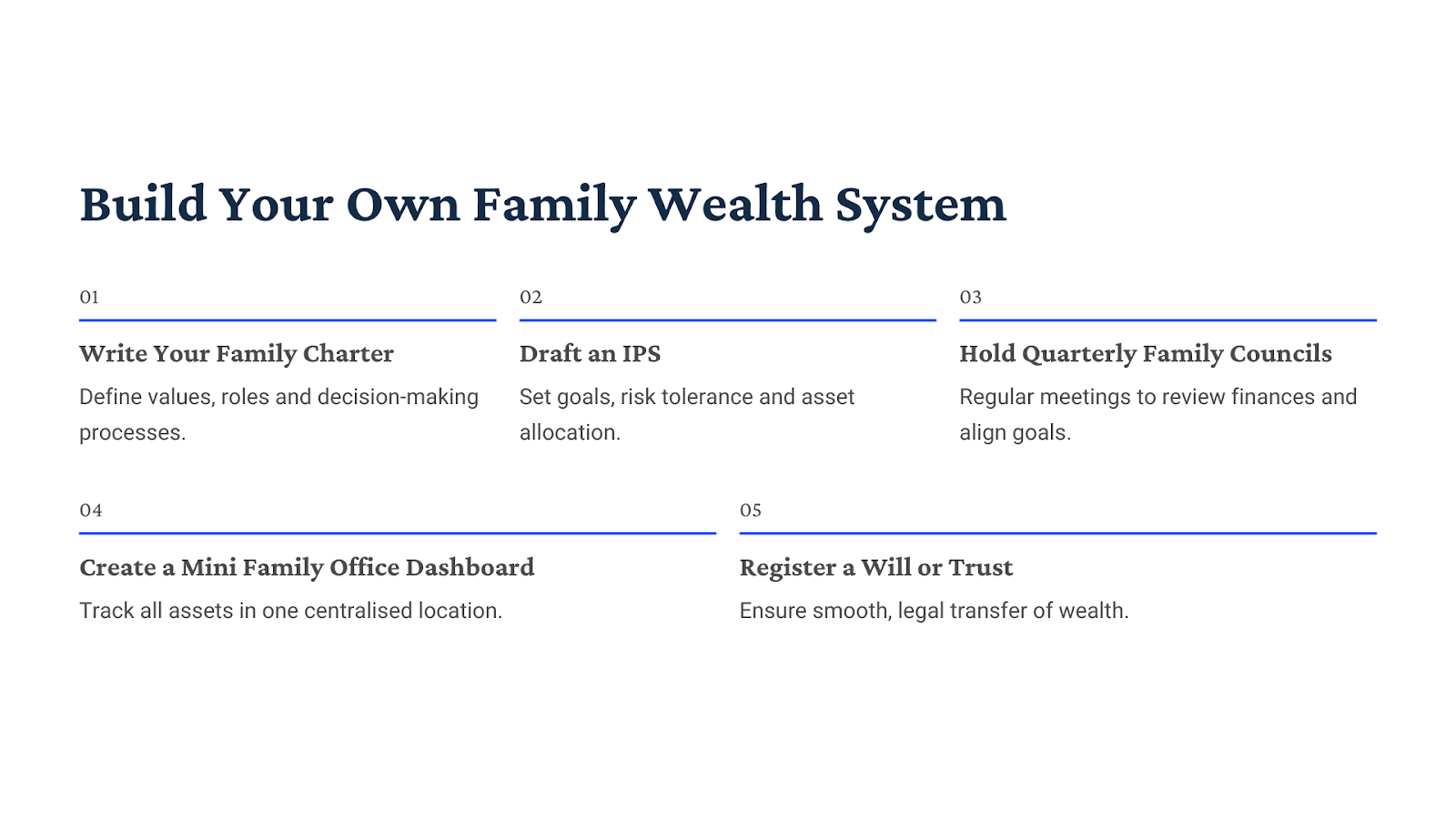

How You Can Implement These at Home

You don’t need a family office or billions in assets. You just need structure, discipline, and a few hours of honest effort.Here’s how to start applying the same frameworks the ultra-wealthy rely on for your own household.

The Family Charter

Gather your family and Write down:

What money means to your family (security, freedom, legacy).

Who decides on spending, saving, and big purchases.

How disagreements will be handled (majority, discussion, or veto).

Name it your Family Charter. It’s not a legal document; it’s a clarity document. When emotions rise, it reminds everyone what was agreed in calmer times.

The Investment Policy Statement (IPS)

Open a blank page and answer four questions:

What are your financial goals? (e.g., house, retirement, children’s education)

What returns do you expect realistically each year?

What risk can you tolerate without panic?

How will you divide your money? (e.g., 60% equity, 30% debt, 10% gold)

What are the rebalancing rules

That’s your IPS. Review it once a year, not every time the market moves. It’s your guardrail against emotional investing.

The Family Council

Once every quarter, sit together for a family finance meeting.

Agenda:

Review savings, investments, and goals.

Discuss upcoming needs (education, travel, emergencies).

Teach your kids what’s happening—even simple things like how SIPs work.

It turns silence into structure and money into shared understanding. You’ll be amazed how quickly financial awareness spreads when it becomes a conversation.

The Mini Family Office

You don’t need a private banker. You need a dashboard.Use tools like Excel, INDmoney, ET Money, or a Google Sheet to track all your investments at one place.

Bank balances

Mutual funds and stocks

Loans and EMIs

Insurance policies and maturity dates

Review it monthly. This is your version of a family office—giving you the same visibility billionaires buy with entire teams.

Trusts & Wills

A single legal document can prevent years of confusion. Meet a lawyer or take any online service to draft a registered will today. If your assets are complex or shared across states, explore a simple family trust to hold them securely.

A WILL will tell your loved ones what to do. A trust, if needed, tells them how to do it. Both ensure your wealth serves your intent, not future arguments.

Turning Wealth Into Legacy

Most people chase wealth. The truly wealthy protect it. Earning money is a skill, but preserving it is a system. You don’t need billions to build a legacy. You need clarity, structure, and courage to document what truly matters.

If this message made you pause, that’s a good sign. It means you care not just about growing wealth—but about keeping it.

At Zomint, we’re building a new wealth culture, where structure, clarity, and discipline matter more than hype. Where even everyday investors can think and plan like the ultra-wealthy.

If you found this valuable, share it with someone who’s quietly building their family’s future. Because the greatest gift you can give your loved ones isn’t money, it’s clarity.

If you didn’t wake up tomorrow, would your family know where your money really is?

Would they know which bank accounts exist, where the property papers are kept,

or how to access your investments and insurance ?

Most of us spend our entire lives working to build financial security, yet very few of us stop to think about how that money will be used, protected, or structured so that it lasts beyond our own lifetime.

But a small circle of ultra-wealthy families has quietly solved this puzzle..

At Zomint, we work closely with many of India’s affluent families. We’ve distilled their wealth-preservation frameworks into practical methods that you can use in your daily life.

If you’ve ever wondered how to make your money last beyond your lifetime -> Continue Reading

The Real Reason Wealth Disappears

When people think about losing wealth, they imagine a market crash or a bad investment.

But that’s rarely how fortunes fade.Studies show nearly 70% of families lose wealth by the second generation, and 90% by the third—not because they earned less, but because they never documented how decisions should be made once the founder steps away.

That’s why the rich world treats Wealth Governance as their first line of defence—the invisible system that keeps peace, clarity, and control intact.

What Happens With and Without Structure?

In the world of money, silence is expensive.

When structure is missing, success turns fragile; siblings stop speaking, partners lose trust, and the empire built through decades becomes a courtroom file.

But where structure exists, clarity replaces confusion.Everyone knows their role, follow process as mentioned, and peace becomes the family’s highest return.

That’s the quiet difference between the rich who stay rich, and those who once were.

How the Ultra-Wealthy Do It?

The Family Constitution

For many of India’s ultra-rich families, the Family Constitution is the unwritten law that holds everything together — a document that defines how wealth, power, and purpose flow across generations..

The wealthy don’t rely on goodwill or tradition; they rely on clarity. Every successor knows what’s expected, and no major decision is made without referencing “the charter.”

The Family Office

Every billionaire family eventually builds a Family Office—a private firm managing everything from investments and tax to philanthropy and art.

It functions like a CFO for the family: tracking every account, reconciling statements, preparing consolidated reports. Some even employ analysts, lawyers, and psychologists under one roof.This single step turns chaos into structure.

The Investment Policy Statement (IPS)

An Investment Policy Statement (IPS) is your family’s written guide for managing money.It explains your goals, how you’ll invest, how much risk you can take, when to make changes, etc.

For example,It dictates:

Target returns (say, inflation + 3%).

Maximum drawdown tolerated (for example 20%).

Asset-class limits and liquidity needs.

When markets fall, they don’t call the broker, they open the IPS. It keeps billion-dollar portfolios from reacting emotionally.

The Family Council

Ultra-rich families don’t let money talk only at funerals. They hold quarterly councils, separate from business boardrooms, to review:

Family balance sheets and cash needs.

Education of the next generation.

Philanthropy and legacy projects.

Younger members sit in as observers, learning early how wealth is managed. It institutionalizes communication and keeps emotions from turning into litigation.

Trusts & Wills

The ultra-wealthy never leave inheritance to emotion. They plan every transfer , what goes to whom, when, and how and that to long before it becomes urgent.

They use:

Family Trusts to hold assets across generations.

Buy-sell agreements to manage exits or deaths.

Registered wills that complement the trust structure.

For Ultra Wealthy families, these five frameworks are not fancy paperwork , they’re risk-management systems for money and relationships. Each one converts uncertainty into process, emotion into policy, and wealth into legacy.

How You Can Implement These at Home

You don’t need a family office or billions in assets. You just need structure, discipline, and a few hours of honest effort.Here’s how to start applying the same frameworks the ultra-wealthy rely on for your own household.

The Family Charter

Gather your family and Write down:

What money means to your family (security, freedom, legacy).

Who decides on spending, saving, and big purchases.

How disagreements will be handled (majority, discussion, or veto).

Name it your Family Charter. It’s not a legal document; it’s a clarity document. When emotions rise, it reminds everyone what was agreed in calmer times.

The Investment Policy Statement (IPS)

Open a blank page and answer four questions:

What are your financial goals? (e.g., house, retirement, children’s education)

What returns do you expect realistically each year?

What risk can you tolerate without panic?

How will you divide your money? (e.g., 60% equity, 30% debt, 10% gold)

What are the rebalancing rules

That’s your IPS. Review it once a year, not every time the market moves. It’s your guardrail against emotional investing.

The Family Council

Once every quarter, sit together for a family finance meeting.

Agenda:

Review savings, investments, and goals.

Discuss upcoming needs (education, travel, emergencies).

Teach your kids what’s happening—even simple things like how SIPs work.

It turns silence into structure and money into shared understanding. You’ll be amazed how quickly financial awareness spreads when it becomes a conversation.

The Mini Family Office

You don’t need a private banker. You need a dashboard.Use tools like Excel, INDmoney, ET Money, or a Google Sheet to track all your investments at one place.

Bank balances

Mutual funds and stocks

Loans and EMIs

Insurance policies and maturity dates

Review it monthly. This is your version of a family office—giving you the same visibility billionaires buy with entire teams.

Trusts & Wills

A single legal document can prevent years of confusion. Meet a lawyer or take any online service to draft a registered will today. If your assets are complex or shared across states, explore a simple family trust to hold them securely.

A WILL will tell your loved ones what to do. A trust, if needed, tells them how to do it. Both ensure your wealth serves your intent, not future arguments.

Turning Wealth Into Legacy

Most people chase wealth. The truly wealthy protect it. Earning money is a skill, but preserving it is a system. You don’t need billions to build a legacy. You need clarity, structure, and courage to document what truly matters.

If this message made you pause, that’s a good sign. It means you care not just about growing wealth—but about keeping it.

At Zomint, we’re building a new wealth culture, where structure, clarity, and discipline matter more than hype. Where even everyday investors can think and plan like the ultra-wealthy.

If you found this valuable, share it with someone who’s quietly building their family’s future. Because the greatest gift you can give your loved ones isn’t money, it’s clarity.