Introduction: Why This Matters Now

Every parent works tirelessly to secure their child’s future but here’s the reality most don’t see. By the age of seven, a child’s money habits are already formed. And despite all the love, effort, and resources, most children still grow up financially illiterate.

They can solve math problems in school, but can’t understand interest rates. They learn to spend pocket money, but not how to save or invest it. The result? Studies show that over 80% of families lose their wealth by the next generation.

The Problems Families Face

When families think about wealth transfer, they often assume the real risks of losing wealth are external like volatile markets, high taxes, or bad investment choices. But the reality is different. Over 80 percent of wealth transfer failures stem from poor family communication, unresolved dynamics, and a lack of financial literacy within the next generation.

Parents work hard to build wealth but never explain their decisions, values, or long-term vision with their future generations. When the next generation suddenly inherits, they feel overwhelmed and disconnected from what the money stands for. Without a clear family mission, wealth becomes fragmented. One child might see it as security, another as freedom to spend, and another as a burden. This difference leads to conflict.

This is why the real risk is not markets but mindsets. Families that define what their wealth stands for, and gradually prepare their heirs, give themselves the best chance of building not just fortune, but continuity. And beyond inheritance, financial wisdom is equally essential for individuals to manage their own personal finances responsibly — to avoid debt traps, plan for life goals, and live with financial confidence

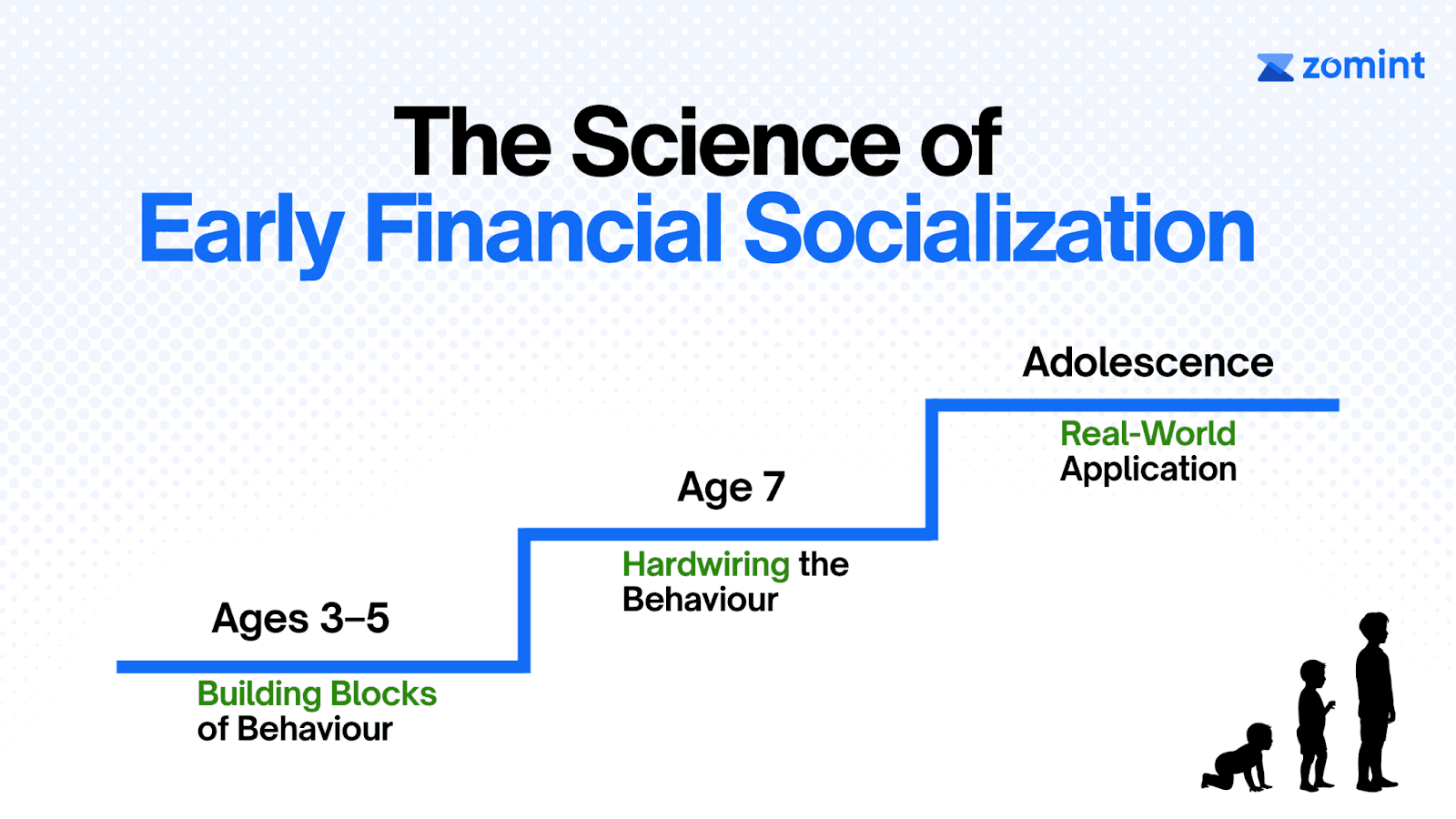

The Science of Early Financial Socialization

So how are these money mindsets actually formed? Science has some clear answers.

The journey to financial wisdom is a gradual one, built on consistent, transparent demonstration over many years. Children are shaped far more by what they observe than by what they are told.

Ages 3–5: The Building Blocks of Behaviour

At this stage, children begin to develop self-control, memory, and habits tied to rewards and consequences. Classic behavioral studies, like the marshmallow test, reveal how early self-regulation strongly predicts future financial well-being. Simple interactions, such as waiting for a turn, saving a small treat for later, or recognizing coins, are the early seeds of money management.

By Age 7: Hardwiring the Behaviour

Research shows that by the age of seven, a child’s money habits are already deeply rooted. The way parents handle saving and spending at home becomes the child’s first reference point. For example, children who regularly see their parents set aside money for short-term needs and long-term goals grow up thinking of saving as natural. On the other hand, children who see impulsive spending or secrecy around money may carry that unease into adulthood, often avoiding financial conversations or feeling anxious about money.

Adolescence: Real-World Application

By the teenage years, talking about financial principles is not enough; young people must be exposed to real-world decision-making. This could be through managing a bank account, handling part-time earnings, or using investment simulators. These experiences provide a safe but practical laboratory where mistakes and learning can occur without long-term damage.

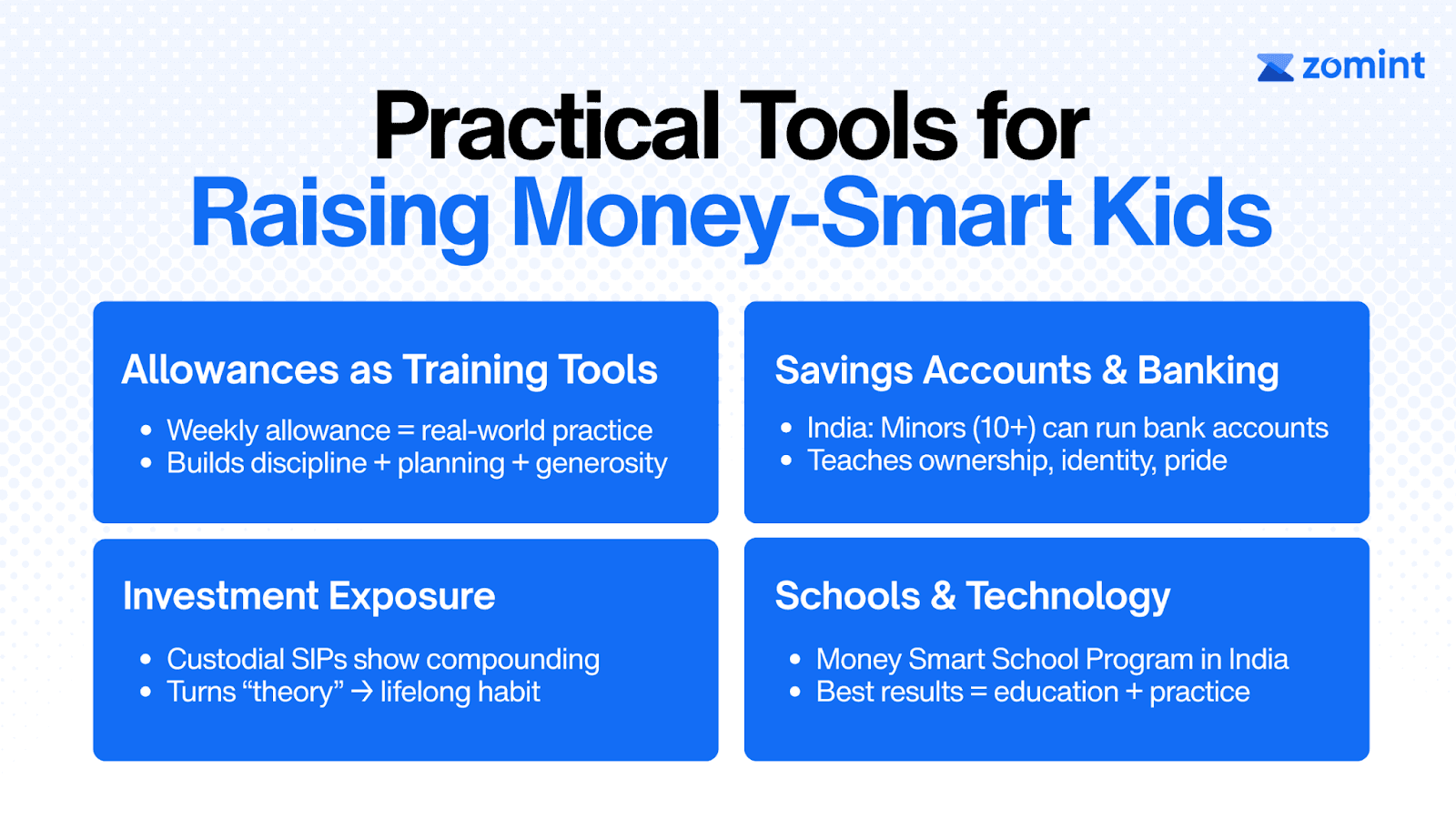

Practical Tools for Raising Money-Smart Kids

Once parents understand the science, the next step is to give children real tools and experiences.

Allowances as Training Tools

Giving children a weekly allowance is one of the simplest and most powerful ways to teach responsibility. The Rockefeller family used this approach for more than six generations, asking children to divide their allowance into three parts: spending, saving, and giving. This routine taught them discipline, future planning, and generosity.

If one of the wealthiest families in the world trusted this system to pass on values, it’s a model worth implementing in our daily life also.

Savings Accounts and Banking

One of the most successful projects ever was the YouthSave Project that gave over 130,000 teenagers in countries such as Ghana, Kenya, Colombia, and Nepal access to real savings accounts. Supported by schools and community programs, the children collectively saved almost $1.8 million and, more importantly, developed a sense of pride and discipline.

In India, the RBI now allows minors above the age of 10 to operate savings accounts under supervision. These accounts come with safeguards like no overdrafts, making them safe to use. The lesson is not just about money saved but about ownership, discipline, and identity.

Investment Exposure

A custodial SIP or education-focused investment account helps children see compounding and volatility in action. Reviewing statements together makes abstract concepts real. It turns investing from a theory into a habit of patience and long-term thinking.

Schools and Technology

India’s Money Smart School Program has brought financial education into classrooms. At home, this learning can be reinforced with modern tools. Families that combine structured education with practical exposure see the strongest results.

These tools work anywhere in the world. But in India, the stakes — and the opportunities — are even bigger.

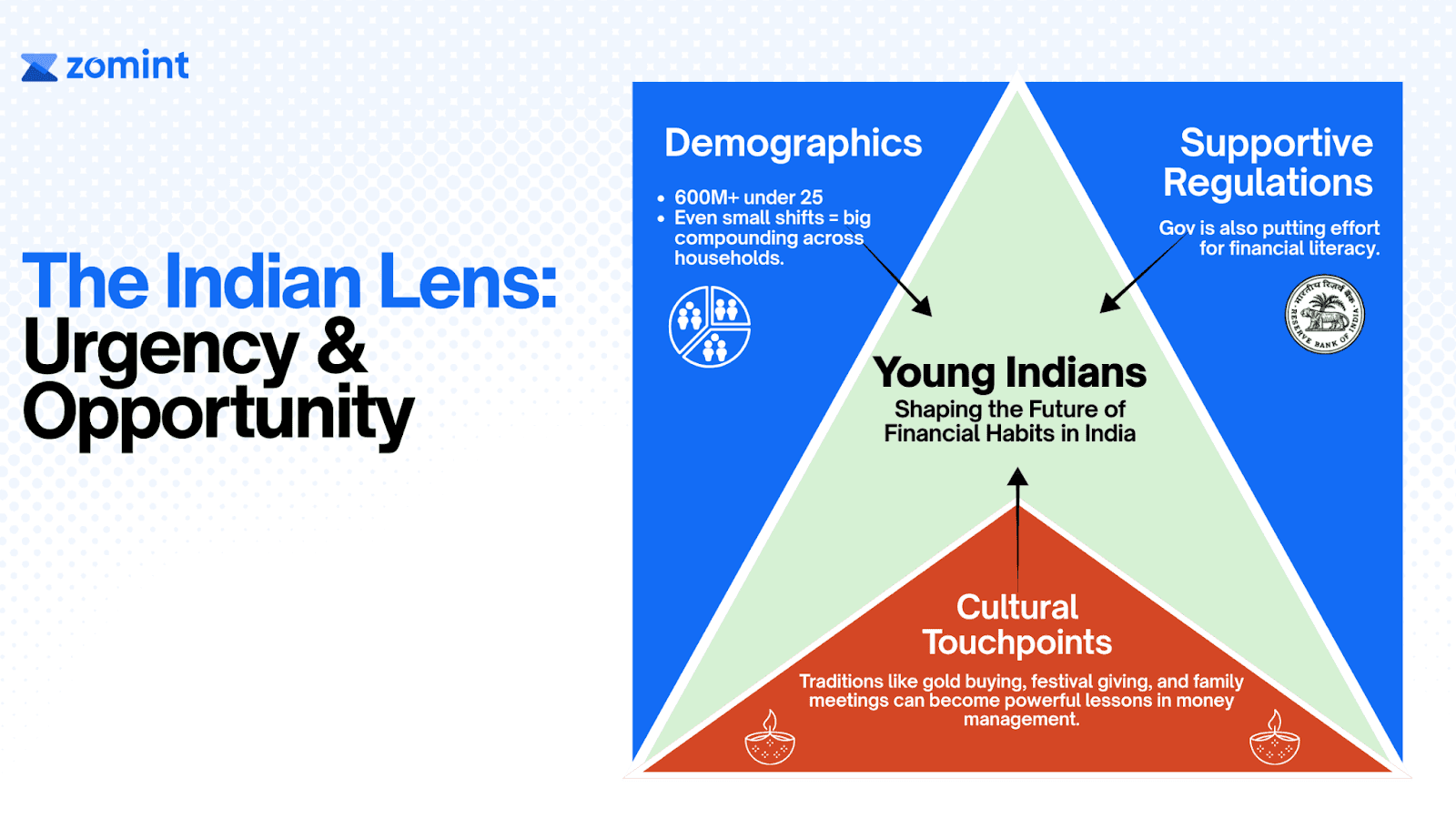

The Indian Lens: Urgency and Opportunity

India is at a turning point. With nearly 600 million young people under 25, the financial habits we cultivate today will decide not just family legacies, but the nation’s economic future. The opportunity is massive here.

What makes this the right moment? Three forces are aligning at once:

Demographics: A huge youth population means even small improvements in saving and investing habits can create a compounding effect across millions of households.

Supportive Regulations: The RBI now allows children as young as 10 to run savings accounts under supervision. SEBI permits minors to hold mutual fund folios. And under the National Strategy for Financial Education (NSFE 2020–25), financial literacy for youth is a formal priority backed by all major regulators.

Cultural Touchpoints: Our traditions already offer natural teaching moments. Gold buying during Diwali or Akshaya Tritiya can spark conversations about assets versus consumption.As families shift from joint to nuclear setups, intentional ‘family money meetings’ can help children continue learning important money lessons.

Together, these three forces give India a once-in-a-generation opportunity to raise money-smart citizens. And when the environment is this supportive, the only missing link is action at the family level.

Conclusion

Financial wisdom is not inherited; it is cultivated. Families that preserve wealth across generations are those that deliberately invest in their children’s financial capability, communication skills, and values.

The goal is not just to raise children who can earn well, but to raise adults who can also manage both their family’s wealth and their own money wisely. The best time to start is now, because by the time children become teenagers, their financial habits are already formed.

Introduction: Why This Matters Now

Every parent works tirelessly to secure their child’s future but here’s the reality most don’t see. By the age of seven, a child’s money habits are already formed. And despite all the love, effort, and resources, most children still grow up financially illiterate.

They can solve math problems in school, but can’t understand interest rates. They learn to spend pocket money, but not how to save or invest it. The result? Studies show that over 80% of families lose their wealth by the next generation.

The Problems Families Face

When families think about wealth transfer, they often assume the real risks of losing wealth are external like volatile markets, high taxes, or bad investment choices. But the reality is different. Over 80 percent of wealth transfer failures stem from poor family communication, unresolved dynamics, and a lack of financial literacy within the next generation.

Parents work hard to build wealth but never explain their decisions, values, or long-term vision with their future generations. When the next generation suddenly inherits, they feel overwhelmed and disconnected from what the money stands for. Without a clear family mission, wealth becomes fragmented. One child might see it as security, another as freedom to spend, and another as a burden. This difference leads to conflict.

This is why the real risk is not markets but mindsets. Families that define what their wealth stands for, and gradually prepare their heirs, give themselves the best chance of building not just fortune, but continuity. And beyond inheritance, financial wisdom is equally essential for individuals to manage their own personal finances responsibly — to avoid debt traps, plan for life goals, and live with financial confidence

The Science of Early Financial Socialization

So how are these money mindsets actually formed? Science has some clear answers.

The journey to financial wisdom is a gradual one, built on consistent, transparent demonstration over many years. Children are shaped far more by what they observe than by what they are told.

Ages 3–5: The Building Blocks of Behaviour

At this stage, children begin to develop self-control, memory, and habits tied to rewards and consequences. Classic behavioral studies, like the marshmallow test, reveal how early self-regulation strongly predicts future financial well-being. Simple interactions, such as waiting for a turn, saving a small treat for later, or recognizing coins, are the early seeds of money management.

By Age 7: Hardwiring the Behaviour

Research shows that by the age of seven, a child’s money habits are already deeply rooted. The way parents handle saving and spending at home becomes the child’s first reference point. For example, children who regularly see their parents set aside money for short-term needs and long-term goals grow up thinking of saving as natural. On the other hand, children who see impulsive spending or secrecy around money may carry that unease into adulthood, often avoiding financial conversations or feeling anxious about money.

Adolescence: Real-World Application

By the teenage years, talking about financial principles is not enough; young people must be exposed to real-world decision-making. This could be through managing a bank account, handling part-time earnings, or using investment simulators. These experiences provide a safe but practical laboratory where mistakes and learning can occur without long-term damage.

Practical Tools for Raising Money-Smart Kids

Once parents understand the science, the next step is to give children real tools and experiences.

Allowances as Training Tools

Giving children a weekly allowance is one of the simplest and most powerful ways to teach responsibility. The Rockefeller family used this approach for more than six generations, asking children to divide their allowance into three parts: spending, saving, and giving. This routine taught them discipline, future planning, and generosity.

If one of the wealthiest families in the world trusted this system to pass on values, it’s a model worth implementing in our daily life also.

Savings Accounts and Banking

One of the most successful projects ever was the YouthSave Project that gave over 130,000 teenagers in countries such as Ghana, Kenya, Colombia, and Nepal access to real savings accounts. Supported by schools and community programs, the children collectively saved almost $1.8 million and, more importantly, developed a sense of pride and discipline.

In India, the RBI now allows minors above the age of 10 to operate savings accounts under supervision. These accounts come with safeguards like no overdrafts, making them safe to use. The lesson is not just about money saved but about ownership, discipline, and identity.

Investment Exposure

A custodial SIP or education-focused investment account helps children see compounding and volatility in action. Reviewing statements together makes abstract concepts real. It turns investing from a theory into a habit of patience and long-term thinking.

Schools and Technology

India’s Money Smart School Program has brought financial education into classrooms. At home, this learning can be reinforced with modern tools. Families that combine structured education with practical exposure see the strongest results.

These tools work anywhere in the world. But in India, the stakes — and the opportunities — are even bigger.

The Indian Lens: Urgency and Opportunity

India is at a turning point. With nearly 600 million young people under 25, the financial habits we cultivate today will decide not just family legacies, but the nation’s economic future. The opportunity is massive here.

What makes this the right moment? Three forces are aligning at once:

Demographics: A huge youth population means even small improvements in saving and investing habits can create a compounding effect across millions of households.

Supportive Regulations: The RBI now allows children as young as 10 to run savings accounts under supervision. SEBI permits minors to hold mutual fund folios. And under the National Strategy for Financial Education (NSFE 2020–25), financial literacy for youth is a formal priority backed by all major regulators.

Cultural Touchpoints: Our traditions already offer natural teaching moments. Gold buying during Diwali or Akshaya Tritiya can spark conversations about assets versus consumption.As families shift from joint to nuclear setups, intentional ‘family money meetings’ can help children continue learning important money lessons.