What if, on your child’s 18th birthday, you handed them ₹1 crore?

No student loans. No financial pressure. Just the freedom to study wherever they want, build something of their own, or step into adulthood with confidence. It sounds like a dream for many parents.But here’s the uncomfortable truth: ₹1 crore, 18 years from now, will be worth only ₹35 lakh in today’s terms.That means the amount you’re planning for today may fall far short of what your child will truly need in the future.

If Not ₹1 Crore, Then How Much?

Most parents aim to save ₹1 crore for their child’s future. But with inflation averaging 6% a year, that will shrink to about ₹35 lakh in today’s terms,not enough to cover even one major milestone like higher education, let alone multiple goals. To match the buying power of ₹1 crore today, you’ll need to target around ₹3 crore over the next 18 years, and even that could feel tight once future costs are factored in.

An engineering degree that costs ₹15 lakh today may rise to ₹60 lakh, while an MBBS could jump from ₹50 lakh to ₹2.5 crore. A foreign degree might demand ₹3–5 crore, and a wedding priced at ₹35 lakh today could reach ₹1.45 crore in the next two decades.

Inflation is the silent factor eroding your savings. The sooner you adjust your target, the better chance you have of fully funding your child’s dreams.

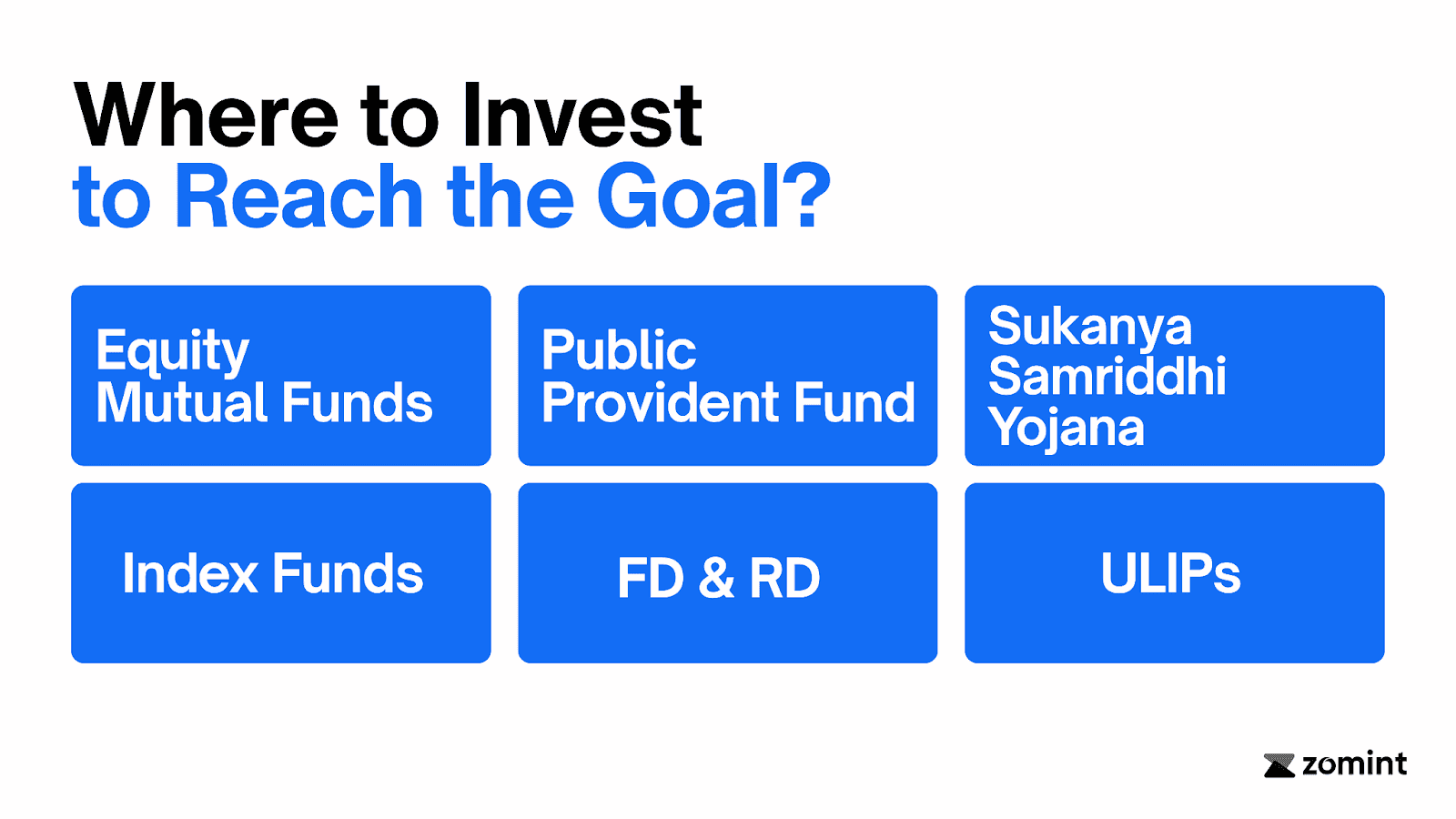

Where should you invest to reach that goal?

To reach your goal , you need time, discipline, and a thoughtful mix of investment tools. Let’s unpack the most effective options available to Indian parents today.

Equity Mutual Funds (via SIPs)

If there's one vehicle that can realistically turn your ₹5,000–₹10,000 monthly investment into crores over 15–20 years, it’s this. Over long periods, equity mutual funds have delivered 12–15% average annual returns, especially when left untouched for over a decade. Even if we assume a more conservative 10–12%, the results can be dramatic and more importantly, they often outpace inflation.

Caution - Equity is volatile in the short term. You must not panic during market dips, and ideally, shift gradually to safer assets as the goal approaches.

Public Provident Fund (PPF)

If equity is the accelerator that drives your wealth forward, PPF is the brake that keeps your plan stable on sharp turns. The Public Provident Fund is one of India’s most trusted long-term saving schemes backed by the Government of India, offering 7.1% tax-free interest (as of now), with EEE status (your investment, interest, and maturity amount are all tax-exempt).

Caution - PPF alone won’t help you reach ₹1 crore. But as a foundation, especially when combined with equity, it’s invaluable.

Sukanya Samriddhi Yojana (SSY)

If you have a daughter below the age of 10, SSY should almost be a default choice. It offers one of the highest risk-free returns among small savings schemes currently at 8.2% per annum, tax-free. The maturity period is 21 years from account opening, which aligns beautifully with child-focused goals.

Caution- There’s an annual contribution cap of ₹1.5 lakh, and you can’t withdraw freely. Use it only for long-term, non-negotiable goals like education or marriage.

Index Funds

Index funds are a subset of equity mutual funds but instead of being actively managed by a fund manager, they simply track the performance of a market index, like the Nifty 50 or Sensex. The advantage? Low cost, broad diversification, and performance that often beats expensive actively-managed funds over the long term.

Caution- Just like equity MFs, these carry market risk. Returns aren’t guaranteed but historically, Nifty/Sensex have grown wealth remarkably over 20+ year periods.

Fixed Deposits (FDs) and Recurring Deposits (RDs)

Most Indian parents instinctively turn to FDs or RDs because they feel familiar, safe, and simple. But over 15–20 years, these instruments barely keep up with inflation. Even a “high” FD rate of 7% gets taxed — and in higher tax brackets, your real return could drop to 4.8–5%, which is less than inflation.

Caution- Don’t rely on FDs to build a ₹1 crore corpus unless you're investing massive amounts — and are okay with eroding real returns.

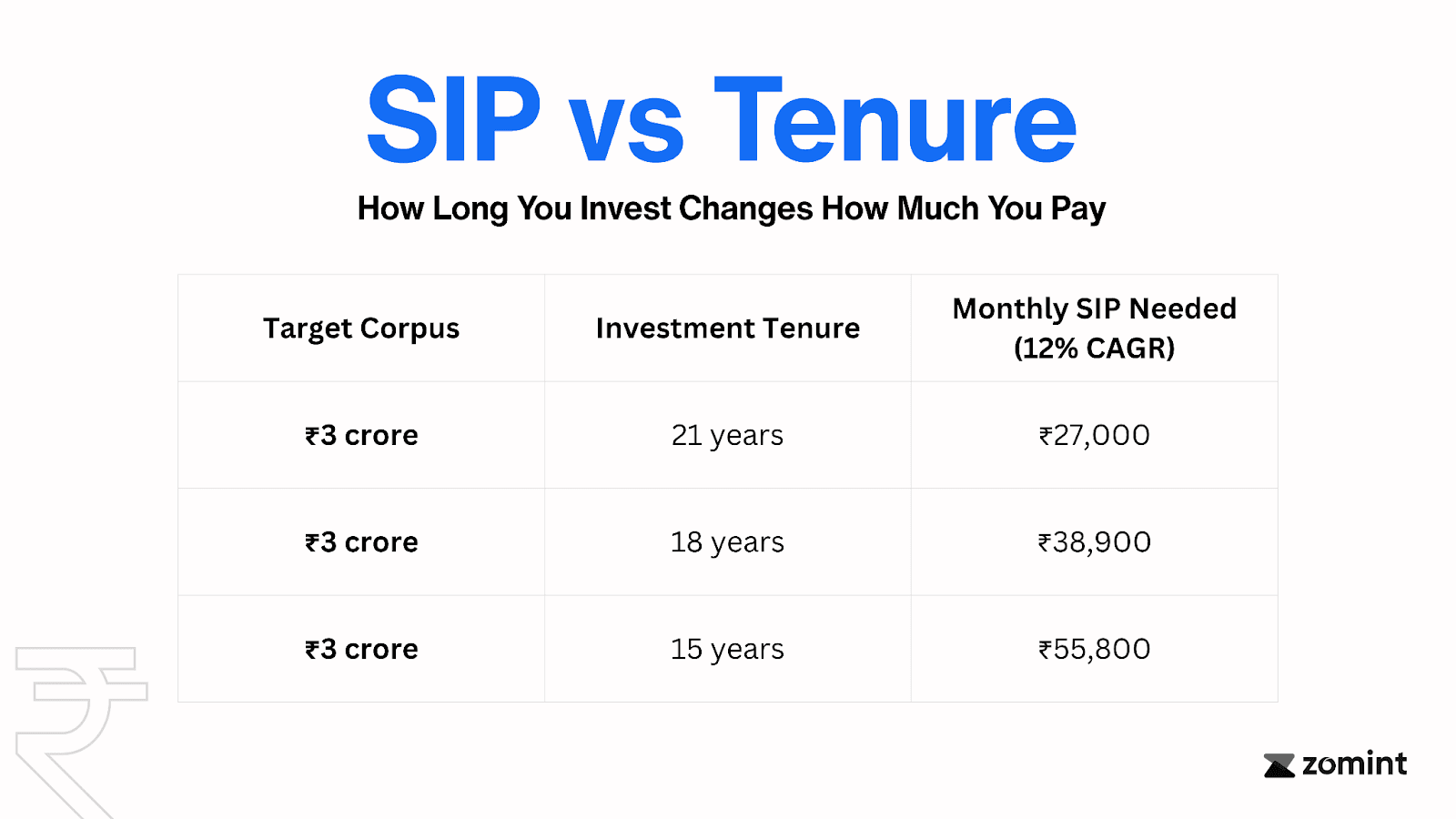

How Much Should You Invest to Reach the Real Goal?

A Systematic Investment Plan (SIP) in equity mutual funds is one of the most effective ways to build long-term wealth for your child. Over a 15–20 year horizon, a well-diversified SIP can deliver average annual returns of 10–12%, comfortably beating inflation and growing your savings into a sizable corpus.

But the challenge here is that, for building a future corpus of around ₹3.4 crore, the monthly SIP often is very high and on top of that, If you start late or have fewer years to invest, this monthly amount rises even further. For many parents, committing ₹30,000 to ₹40,000 per month from the very beginning is simply not practical. So what to do now ?

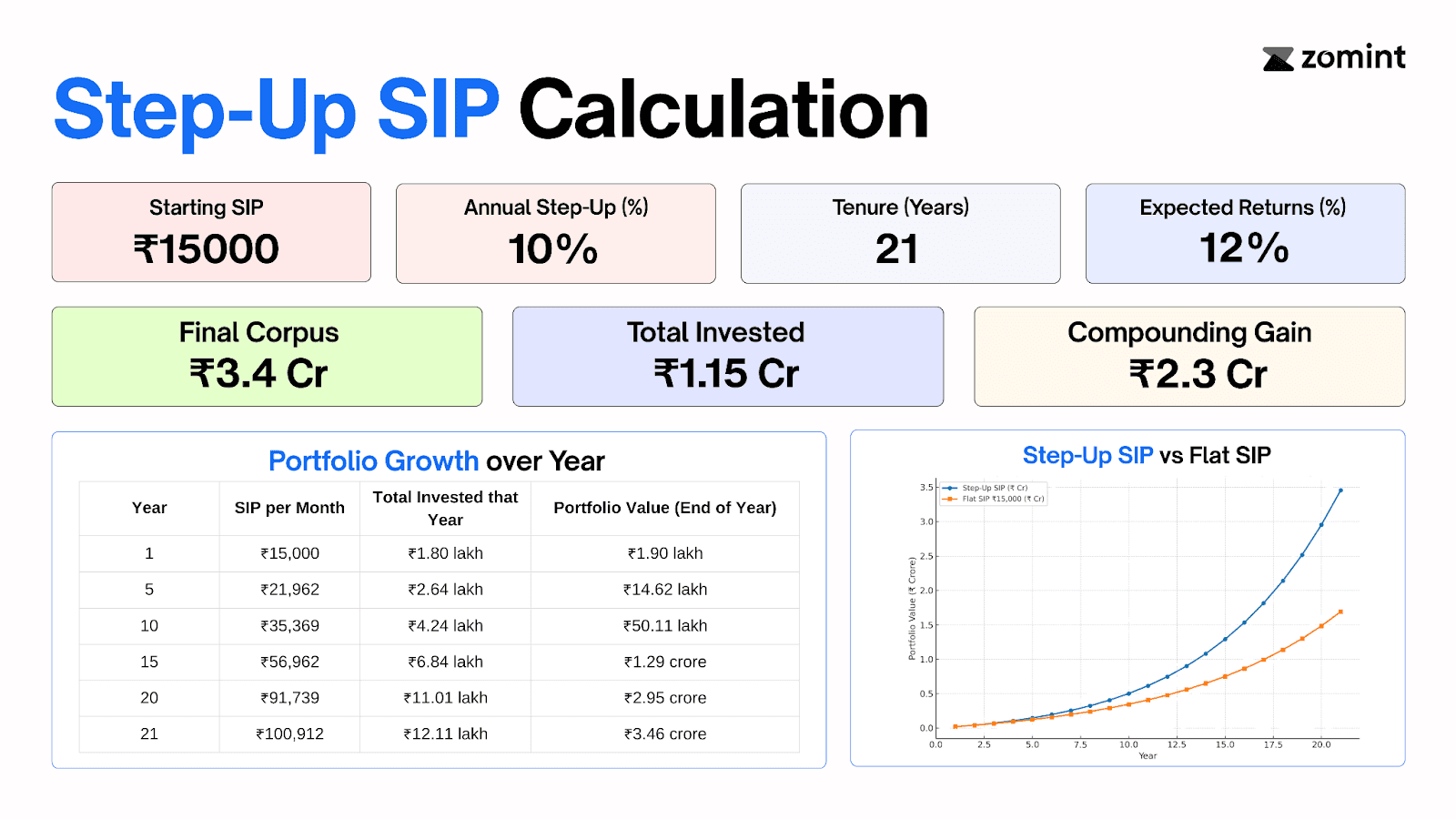

That’s where Step-Up SIPs come in. Instead of investing a large sum of money from day one, you begin with a comfortable amount and increase your SIP each year (usually by 10%), as your income grows. This approach helps to keep your budget flexible in the early years while allowing compounding to work its magic over time.

The Power of a Step-Up SIP

A Step-Up SIP works just like a regular SIP, but with one key difference, and that is you can increase your monthly investment each year, usually by a fixed percentage, which is again proportional with your income growth.

To show you the power of a Step-Up SIP, let’s look at an example.

We have assumed a starting SIP of ₹15,000 per month, a 10% annual increase in the SIP amount, an investment period of 21 years, and annual returns of 12% with monthly compounding.

Over 21 years, you would invest a total of about ₹1.15 crore. In the same period, this could grow into a corpus of roughly ₹3.46 crore ,with ₹2.30 crore of that coming purely from compounding. The best part is, you can achieve this without the burden of starting with a very large monthly amount.

Follow the infographics below to get a better understanding of Step-Up SIP and how it's better than your regular SIPs.

Whether you choose a regular SIP or a Step-Up SIP, the next step is deciding how to spread that investment across different tools based on your goals, risk comfort, and the level of involvement you want in managing it.

How to Build Your Own Plan ?

There’s no single “perfect” plan for everyone. Every parent's needs and risk profile is different. The right mix depends on various factors such as how much risk you’re comfortable taking and how actively you want to manage your investments.

If you prioritise safety then focus on instruments like PPF, Sukanya Samriddhi Yojana (for daughters), and bank deposits (FDs & RDs). These offer guaranteed returns, some tax benefits, and peace of mind, though they grow slower and often fail to beat inflation.

If you want balanced growth, combine equity mutual funds (through SIPs) with safe options like PPF or gold ETFs. This gives you enough growth to beat inflation while keeping part of your money stable.

If you’re comfortable taking higher risks and can stay invested for the long term, consider allocating more to SIPs in equity mutual funds. As your child approaches the age of 18 or 21, gradually shift the funds into safer options to protect them from market fluctuations.

Your 3-Step Blueprint to Your Child’s Crorepati Future

If you’ve read this far, you already have what most parents don't have,clarity and intent. Now all that’s left is execution. Here’s the 3-step blueprint to secure your child’s future

Start Early and Stay Consistent – Begin SIPs as soon as possible. Even ₹5,000 a month can grow significantly over 18–21 years. Increase contributions as your income grows.

Mix Growth and Stability – Use equity SIPs for higher growth, SSY or PPF for safety, and gold ETFs or debt funds for diversification.

Secure the Plan – A term insurance policy of ₹1 crore+ protects your child’s future if something unexpected happens. Nominate every investment and keep the plan simple enough for your family to follow.

Want a Plan That Actually Works for Your Child?

Talk to our SEBI-registered experts and get a personalised investment plan for your child’s future tailored to your risk comfort, goals, and timeline. Whether you’re aiming for ₹1 crore or ₹5 crore, we’ll help you pick the right mix of investments and guide you every step of the way.

Book your child investment planning session now at zomint.com

Disclaimer:

This article is for educational and informational purposes only. It does not constitute financial, investment, or tax advice. All investments are subject to market risks. Please consult a SEBI-registered investment advisor before making any financial decisions.

What if, on your child’s 18th birthday, you handed them ₹1 crore?

No student loans. No financial pressure. Just the freedom to study wherever they want, build something of their own, or step into adulthood with confidence. It sounds like a dream for many parents.But here’s the uncomfortable truth: ₹1 crore, 18 years from now, will be worth only ₹35 lakh in today’s terms.That means the amount you’re planning for today may fall far short of what your child will truly need in the future.

If Not ₹1 Crore, Then How Much?

Most parents aim to save ₹1 crore for their child’s future. But with inflation averaging 6% a year, that will shrink to about ₹35 lakh in today’s terms,not enough to cover even one major milestone like higher education, let alone multiple goals. To match the buying power of ₹1 crore today, you’ll need to target around ₹3 crore over the next 18 years, and even that could feel tight once future costs are factored in.

An engineering degree that costs ₹15 lakh today may rise to ₹60 lakh, while an MBBS could jump from ₹50 lakh to ₹2.5 crore. A foreign degree might demand ₹3–5 crore, and a wedding priced at ₹35 lakh today could reach ₹1.45 crore in the next two decades.

Inflation is the silent factor eroding your savings. The sooner you adjust your target, the better chance you have of fully funding your child’s dreams.

Where should you invest to reach that goal?

To reach your goal , you need time, discipline, and a thoughtful mix of investment tools. Let’s unpack the most effective options available to Indian parents today.

Equity Mutual Funds (via SIPs)

If there's one vehicle that can realistically turn your ₹5,000–₹10,000 monthly investment into crores over 15–20 years, it’s this. Over long periods, equity mutual funds have delivered 12–15% average annual returns, especially when left untouched for over a decade. Even if we assume a more conservative 10–12%, the results can be dramatic and more importantly, they often outpace inflation.

Caution - Equity is volatile in the short term. You must not panic during market dips, and ideally, shift gradually to safer assets as the goal approaches.

Public Provident Fund (PPF)

If equity is the accelerator that drives your wealth forward, PPF is the brake that keeps your plan stable on sharp turns. The Public Provident Fund is one of India’s most trusted long-term saving schemes backed by the Government of India, offering 7.1% tax-free interest (as of now), with EEE status (your investment, interest, and maturity amount are all tax-exempt).

Caution - PPF alone won’t help you reach ₹1 crore. But as a foundation, especially when combined with equity, it’s invaluable.

Sukanya Samriddhi Yojana (SSY)

If you have a daughter below the age of 10, SSY should almost be a default choice. It offers one of the highest risk-free returns among small savings schemes currently at 8.2% per annum, tax-free. The maturity period is 21 years from account opening, which aligns beautifully with child-focused goals.

Caution- There’s an annual contribution cap of ₹1.5 lakh, and you can’t withdraw freely. Use it only for long-term, non-negotiable goals like education or marriage.

Index Funds

Index funds are a subset of equity mutual funds but instead of being actively managed by a fund manager, they simply track the performance of a market index, like the Nifty 50 or Sensex. The advantage? Low cost, broad diversification, and performance that often beats expensive actively-managed funds over the long term.

Caution- Just like equity MFs, these carry market risk. Returns aren’t guaranteed but historically, Nifty/Sensex have grown wealth remarkably over 20+ year periods.

Fixed Deposits (FDs) and Recurring Deposits (RDs)

Most Indian parents instinctively turn to FDs or RDs because they feel familiar, safe, and simple. But over 15–20 years, these instruments barely keep up with inflation. Even a “high” FD rate of 7% gets taxed — and in higher tax brackets, your real return could drop to 4.8–5%, which is less than inflation.

Caution- Don’t rely on FDs to build a ₹1 crore corpus unless you're investing massive amounts — and are okay with eroding real returns.

How Much Should You Invest to Reach the Real Goal?

A Systematic Investment Plan (SIP) in equity mutual funds is one of the most effective ways to build long-term wealth for your child. Over a 15–20 year horizon, a well-diversified SIP can deliver average annual returns of 10–12%, comfortably beating inflation and growing your savings into a sizable corpus.

But the challenge here is that, for building a future corpus of around ₹3.4 crore, the monthly SIP often is very high and on top of that, If you start late or have fewer years to invest, this monthly amount rises even further. For many parents, committing ₹30,000 to ₹40,000 per month from the very beginning is simply not practical. So what to do now ?

That’s where Step-Up SIPs come in. Instead of investing a large sum of money from day one, you begin with a comfortable amount and increase your SIP each year (usually by 10%), as your income grows. This approach helps to keep your budget flexible in the early years while allowing compounding to work its magic over time.

The Power of a Step-Up SIP

A Step-Up SIP works just like a regular SIP, but with one key difference, and that is you can increase your monthly investment each year, usually by a fixed percentage, which is again proportional with your income growth.

To show you the power of a Step-Up SIP, let’s look at an example.

We have assumed a starting SIP of ₹15,000 per month, a 10% annual increase in the SIP amount, an investment period of 21 years, and annual returns of 12% with monthly compounding.

Over 21 years, you would invest a total of about ₹1.15 crore. In the same period, this could grow into a corpus of roughly ₹3.46 crore ,with ₹2.30 crore of that coming purely from compounding. The best part is, you can achieve this without the burden of starting with a very large monthly amount.

Follow the infographics below to get a better understanding of Step-Up SIP and how it's better than your regular SIPs.

Whether you choose a regular SIP or a Step-Up SIP, the next step is deciding how to spread that investment across different tools based on your goals, risk comfort, and the level of involvement you want in managing it.

How to Build Your Own Plan ?

There’s no single “perfect” plan for everyone. Every parent's needs and risk profile is different. The right mix depends on various factors such as how much risk you’re comfortable taking and how actively you want to manage your investments.

If you prioritise safety then focus on instruments like PPF, Sukanya Samriddhi Yojana (for daughters), and bank deposits (FDs & RDs). These offer guaranteed returns, some tax benefits, and peace of mind, though they grow slower and often fail to beat inflation.

If you want balanced growth, combine equity mutual funds (through SIPs) with safe options like PPF or gold ETFs. This gives you enough growth to beat inflation while keeping part of your money stable.

If you’re comfortable taking higher risks and can stay invested for the long term, consider allocating more to SIPs in equity mutual funds. As your child approaches the age of 18 or 21, gradually shift the funds into safer options to protect them from market fluctuations.

Your 3-Step Blueprint to Your Child’s Crorepati Future

If you’ve read this far, you already have what most parents don't have,clarity and intent. Now all that’s left is execution. Here’s the 3-step blueprint to secure your child’s future

Start Early and Stay Consistent – Begin SIPs as soon as possible. Even ₹5,000 a month can grow significantly over 18–21 years. Increase contributions as your income grows.

Mix Growth and Stability – Use equity SIPs for higher growth, SSY or PPF for safety, and gold ETFs or debt funds for diversification.

Secure the Plan – A term insurance policy of ₹1 crore+ protects your child’s future if something unexpected happens. Nominate every investment and keep the plan simple enough for your family to follow.

Want a Plan That Actually Works for Your Child?

Talk to our SEBI-registered experts and get a personalised investment plan for your child’s future tailored to your risk comfort, goals, and timeline. Whether you’re aiming for ₹1 crore or ₹5 crore, we’ll help you pick the right mix of investments and guide you every step of the way.

Book your child investment planning session now at zomint.com

Disclaimer:

This article is for educational and informational purposes only. It does not constitute financial, investment, or tax advice. All investments are subject to market risks. Please consult a SEBI-registered investment advisor before making any financial decisions.